Fabrib

Forumer storico

Brazil Could Be Headed For A Slow Recovery

Jun. 12, 2016 7:39 AM ET

|

About: iShares MSCI Brazil Capped ETF (EWZ)

Quinn Foley

⊕Follow(138 followers)

Long/short equity, macro, foreign companies, bonds

Send Message

|

Madison Investment Research

Summary

Brazil, mired in economic headwinds and scandal, recently voted to impeach President Rousseff.

Michel Temer's plan to freeze public spending and privatize business is just what the economy needs.

If Temer's plan passes, the foundation will be in place to drive a slow recovery.

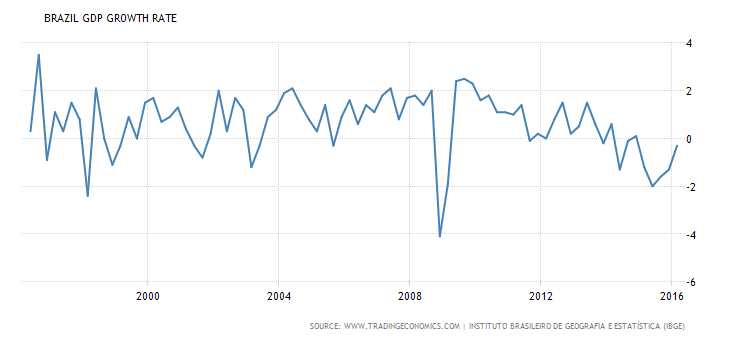

Brazil is in the midst of its worst recession in perhaps its entire history. According to The Economist, real GDP contracted 0.3% in the first quarter, on top of last year's 5.4% decrease in same period. The economy is engulfed in a hurricane of headwinds. Low commodity prices have weighed on Brazil's export sectors, decreased government revenues, and created inflation. At the same time the government has overspent on social programs and outsized pension systems that it can't afford. Credit downgrades to the country's sovereign bonds have driven up the cost of servicing its large debt. And the massive corruption scandal involving Petrobras (NYSE:PBR) and government officials (which lead to Dilma Rousseff's impeachment) has crushed business sentiment.

Rousseff's temporary replacement, Michel Temer, is tasked with sparking an economic recovery in Brazil. It may seem that, because not much more could possible go wrong for the economy, it could only improve. While it is somewhat true that the economy would gradually adjust and improve on its own accord, excess regulation and government meddling in the private sector complicate this natural "shake-out" process. Mr. Temer's plan gives us confidence that Brazil is on its way up. He proposes much needed reforms, including public spending and pension cuts, easing regulations in the oil and gas sector, and an overhaul of the country's archaic labor laws that stymie growth. The move towards privatization is a complete reversal from the state interventionist model that characterized Ms. Rousseff's government. But reducing the role of government in the economy is a necessary step, as it was a bloated public sector that got Brazil into this mess in the first place.

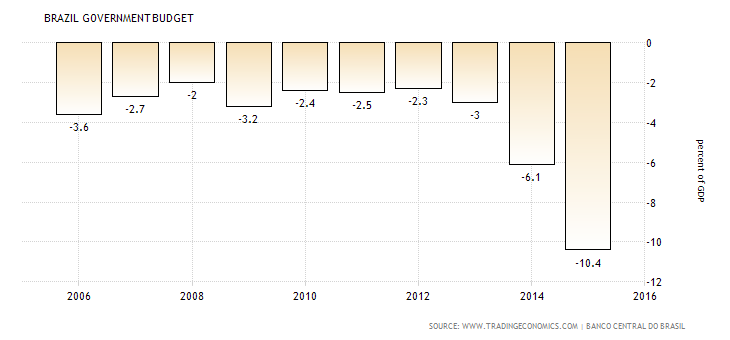

Government spending grew at a 6% annual CAGR over the past 20 years, compared to GDP growth of 2.8% (according to tradingeconomics.com). Spending at double the rate of value produced is not sustainable, and the government's fiscal balance predictably deteriorated (Figure 2). According to The Economist, the primary fiscal balance (before interest payments) went from a surplus of 2.2% of GDP in 2010 to a deficit of 2.3% in April 2016. Deficit spending has pushed up interest rates making it costlier to service the debt. In the last year alone, the net budget shortfall increased from 6.1% of GDP to 10.4%. At the end of 2015, gross debt stood at 66% of GDP, compared to 57% in 2014. In order to finance these deficits, the government has raised taxes and crowded out the private sector. Mr. Temer's proposed spending cap will not be a quick fix, but it is a step in the right direction.

Figure 1: GDP Growth 1996 - 2016

(click to enlarge)

Source: tradingeconomics

Figure 2: Net Fiscal Balance

(click to enlarge)

Source: tradingeconomics

Of course, the proposal has to make it through Congress, which is not a guarantee. But if it passes, the foundation will be in place to help drive a slow recovery. The economy still suffers from hangovers of the Petrobras scandal and while confidence is currently low, businesses will eventually return. Contrarian investors can get exposure to Brazil through the iShares MSCI Brazil Index Fund (NYSEARCA:EWZ), which tracks the performance of the country's largest companies. Brazil's main stock market index, the Ibovespa, has rebounded more than 30% from its 52-week low in January, driven by a weaker dollar and a recovery in commodity prices, but it is still down almost 10% for the year. Investors could find value if they wait until the next dip.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Jun. 12, 2016 7:39 AM ET

|

About: iShares MSCI Brazil Capped ETF (EWZ)

Quinn Foley

⊕Follow(138 followers)

Long/short equity, macro, foreign companies, bonds

Send Message

|

Madison Investment Research

Summary

Brazil, mired in economic headwinds and scandal, recently voted to impeach President Rousseff.

Michel Temer's plan to freeze public spending and privatize business is just what the economy needs.

If Temer's plan passes, the foundation will be in place to drive a slow recovery.

Brazil is in the midst of its worst recession in perhaps its entire history. According to The Economist, real GDP contracted 0.3% in the first quarter, on top of last year's 5.4% decrease in same period. The economy is engulfed in a hurricane of headwinds. Low commodity prices have weighed on Brazil's export sectors, decreased government revenues, and created inflation. At the same time the government has overspent on social programs and outsized pension systems that it can't afford. Credit downgrades to the country's sovereign bonds have driven up the cost of servicing its large debt. And the massive corruption scandal involving Petrobras (NYSE:PBR) and government officials (which lead to Dilma Rousseff's impeachment) has crushed business sentiment.

Rousseff's temporary replacement, Michel Temer, is tasked with sparking an economic recovery in Brazil. It may seem that, because not much more could possible go wrong for the economy, it could only improve. While it is somewhat true that the economy would gradually adjust and improve on its own accord, excess regulation and government meddling in the private sector complicate this natural "shake-out" process. Mr. Temer's plan gives us confidence that Brazil is on its way up. He proposes much needed reforms, including public spending and pension cuts, easing regulations in the oil and gas sector, and an overhaul of the country's archaic labor laws that stymie growth. The move towards privatization is a complete reversal from the state interventionist model that characterized Ms. Rousseff's government. But reducing the role of government in the economy is a necessary step, as it was a bloated public sector that got Brazil into this mess in the first place.

Government spending grew at a 6% annual CAGR over the past 20 years, compared to GDP growth of 2.8% (according to tradingeconomics.com). Spending at double the rate of value produced is not sustainable, and the government's fiscal balance predictably deteriorated (Figure 2). According to The Economist, the primary fiscal balance (before interest payments) went from a surplus of 2.2% of GDP in 2010 to a deficit of 2.3% in April 2016. Deficit spending has pushed up interest rates making it costlier to service the debt. In the last year alone, the net budget shortfall increased from 6.1% of GDP to 10.4%. At the end of 2015, gross debt stood at 66% of GDP, compared to 57% in 2014. In order to finance these deficits, the government has raised taxes and crowded out the private sector. Mr. Temer's proposed spending cap will not be a quick fix, but it is a step in the right direction.

Figure 1: GDP Growth 1996 - 2016

(click to enlarge)

Source: tradingeconomics

Figure 2: Net Fiscal Balance

(click to enlarge)

Source: tradingeconomics

Of course, the proposal has to make it through Congress, which is not a guarantee. But if it passes, the foundation will be in place to help drive a slow recovery. The economy still suffers from hangovers of the Petrobras scandal and while confidence is currently low, businesses will eventually return. Contrarian investors can get exposure to Brazil through the iShares MSCI Brazil Index Fund (NYSEARCA:EWZ), which tracks the performance of the country's largest companies. Brazil's main stock market index, the Ibovespa, has rebounded more than 30% from its 52-week low in January, driven by a weaker dollar and a recovery in commodity prices, but it is still down almost 10% for the year. Investors could find value if they wait until the next dip.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.