Stai usando un browser molto obsoleto. Puoi incorrere in problemi di visualizzazione di questo e altri siti oltre che in problemi di sicurezza. .

Dovresti aggiornarlo oppure usarne uno alternativo, moderno e sicuro.

Dovresti aggiornarlo oppure usarne uno alternativo, moderno e sicuro.

Tbond Bund (VM69) 2013: Bandits Unchained tra Krug bubbles and balls

- Creatore Discussione MissT

- Data di Inizio

f4f

翠鸟科

presente.. anche se poco...

anche io per pochissimo,

giornata molto incasinata

peccato perchè per me oggi draghi parla un pò

my 2c:

S&P ribatte il chiodo IMU

a favore di quanto detto da FMI e a supporto di Rehn-EU

f4f

翠鸟科

GGGIIIIPAAAAAA !!

Bruxelles, pronta l’autorità per liquidare le banche

Il commissario Barnier presenta oggi la proposta di direttiva che è già stata criticata dalla Germania

La Commissione presenterà ufficialmente oggi l’atteso progetto legislativo che ha come obiettivo la creazione di una autorità unica europea responsabile della ristrutturazione o del fallimento di una banca in crisi. Pur messa a punto tenendo conto delle diverse posizioni nazionali, la proposta rischia di creare malumore in alcuni paesi, per esempio in Germania. Ieri ancora il ministro delle Finanze tedesco Wolfgang Schäuble ha sottolineato la necessità di trovare formule rispettose dei Trattati.

Il progetto legislativo, un pilastro dell’unione bancaria, si basa su un meccanismo unico di risoluzione delle banche. La Commissione propone la nascita di un consiglio che raggrupperebbe i rappresentanti dell’esecutivo comunitario, della Banca centrale europea e delle autorità nazionali della banca in crisi. Questo organismo istruirebbe la pratica; la decisione finale verrebbe presa dalla Commissione. Nei fatti la ristrutturazione o la chiusura della banca sarebbero gestite a livello nazionale.

Associato al consiglio di risoluzione sarebbe un fondo di risoluzione, indispensabile per finanziare l’eventuale ristrutturazione dell’istituto. Il fondo verrebbe finanziato principalmente da denaro privato, ma anche dai fondi pubblici nazionali attualmente esistenti. L’obiettivo della proposta legislativa è di completare gradualmente l’unione bancaria, associando un solo meccanismo di fallimento creditizio alla vigilanza unica in mano alla Bce dal 2014 in poi.

Bruxelles, pronta l’autorità per liquidare le banche

Il commissario Barnier presenta oggi la proposta di direttiva che è già stata criticata dalla Germania

La Commissione presenterà ufficialmente oggi l’atteso progetto legislativo che ha come obiettivo la creazione di una autorità unica europea responsabile della ristrutturazione o del fallimento di una banca in crisi. Pur messa a punto tenendo conto delle diverse posizioni nazionali, la proposta rischia di creare malumore in alcuni paesi, per esempio in Germania. Ieri ancora il ministro delle Finanze tedesco Wolfgang Schäuble ha sottolineato la necessità di trovare formule rispettose dei Trattati.

Il progetto legislativo, un pilastro dell’unione bancaria, si basa su un meccanismo unico di risoluzione delle banche. La Commissione propone la nascita di un consiglio che raggrupperebbe i rappresentanti dell’esecutivo comunitario, della Banca centrale europea e delle autorità nazionali della banca in crisi. Questo organismo istruirebbe la pratica; la decisione finale verrebbe presa dalla Commissione. Nei fatti la ristrutturazione o la chiusura della banca sarebbero gestite a livello nazionale.

Associato al consiglio di risoluzione sarebbe un fondo di risoluzione, indispensabile per finanziare l’eventuale ristrutturazione dell’istituto. Il fondo verrebbe finanziato principalmente da denaro privato, ma anche dai fondi pubblici nazionali attualmente esistenti. L’obiettivo della proposta legislativa è di completare gradualmente l’unione bancaria, associando un solo meccanismo di fallimento creditizio alla vigilanza unica in mano alla Bce dal 2014 in poi.

gipa69

collegio dei patafisici

GGGIIIIPAAAAAA !!

Bruxelles, pronta l’autorità per liquidare le banche

Il commissario Barnier presenta oggi la proposta di direttiva che è già stata criticata dalla Germania

La Commissione presenterà ufficialmente oggi l’atteso progetto legislativo che ha come obiettivo la creazione di una autorità unica europea responsabile della ristrutturazione o del fallimento di una banca in crisi. Pur messa a punto tenendo conto delle diverse posizioni nazionali, la proposta rischia di creare malumore in alcuni paesi, per esempio in Germania. Ieri ancora il ministro delle Finanze tedesco Wolfgang Schäuble ha sottolineato la necessità di trovare formule rispettose dei Trattati.

Il progetto legislativo, un pilastro dell’unione bancaria, si basa su un meccanismo unico di risoluzione delle banche. La Commissione propone la nascita di un consiglio che raggrupperebbe i rappresentanti dell’esecutivo comunitario, della Banca centrale europea e delle autorità nazionali della banca in crisi. Questo organismo istruirebbe la pratica; la decisione finale verrebbe presa dalla Commissione. Nei fatti la ristrutturazione o la chiusura della banca sarebbero gestite a livello nazionale.

Associato al consiglio di risoluzione sarebbe un fondo di risoluzione, indispensabile per finanziare l’eventuale ristrutturazione dell’istituto. Il fondo verrebbe finanziato principalmente da denaro privato, ma anche dai fondi pubblici nazionali attualmente esistenti. L’obiettivo della proposta legislativa è di completare gradualmente l’unione bancaria, associando un solo meccanismo di fallimento creditizio alla vigilanza unica in mano alla Bce dal 2014 in poi.

gia gia....

")

gipa69

collegio dei patafisici

gipa69

collegio dei patafisici

Argomenti di interesse:

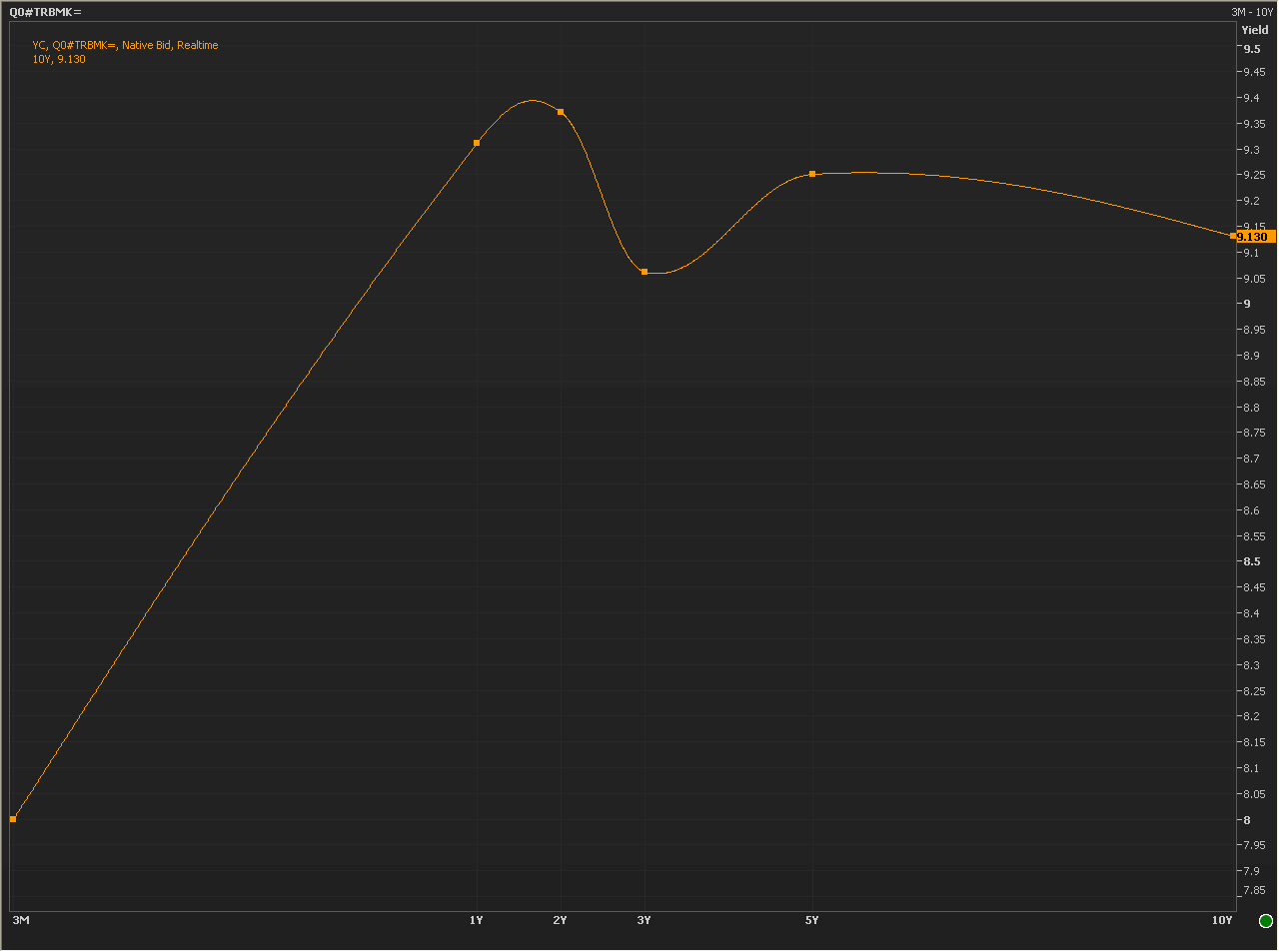

The Turkish inversion

| Jul 10 16:04

That’s the Turkish two-year yield rising above the 10-year earlier on Wednesday — chart via Reuters:

Raise rates, or carry on throwing FX reserves into trying to stop Turkey being the first EM casualty of the great post-Fed shift in global liquidity. (Net reserves of around $47bn, about $3.5bn splurged on interventions this week…)

Hmm. What to do. (Chart via Nomura)

The Turkish inversion

| Jul 10 16:04

That’s the Turkish two-year yield rising above the 10-year earlier on Wednesday — chart via Reuters:

Raise rates, or carry on throwing FX reserves into trying to stop Turkey being the first EM casualty of the great post-Fed shift in global liquidity. (Net reserves of around $47bn, about $3.5bn splurged on interventions this week…)

Hmm. What to do. (Chart via Nomura)

Ultima modifica:

gipa69

collegio dei patafisici

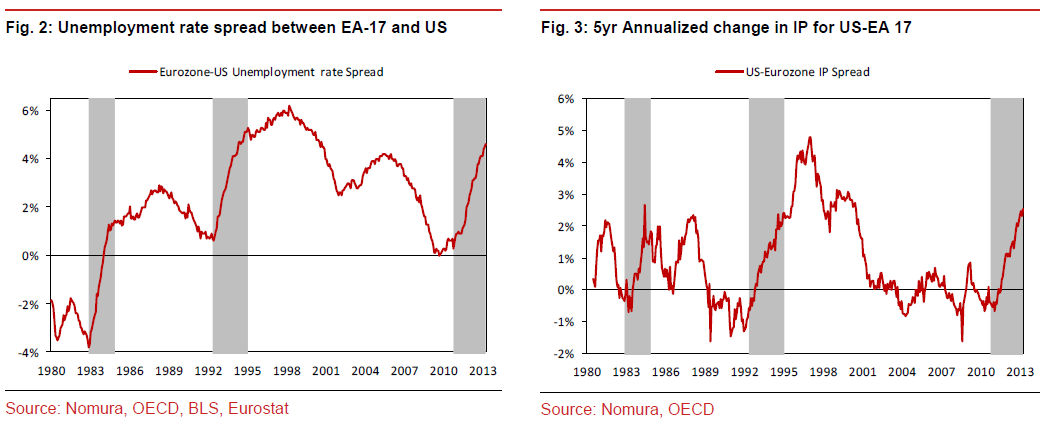

One very large divergence please (with a dollar chaser)

According to Nomura, since 1980, there are only two periods of economic divergence — between the US and Europe and the UK — comparable to what we are observing currently.

The first period was in the early 1980s, when the US unemployment rate peaked in December 1982, but the rate in the UK and Eurozone kept rising beyond this point. This allowed the Fed to start a hiking cycle as early as late-1980, while the BOE was still cutting rates until mid-1981. The impact on the currency market was clear as well, with this helping to exacerbate the broad-based USD rally which continued until the Plaza Accord in 1985. The overall broad USD rally from 1978-85 was more than 50% in real terms.

The second notable divergence was in the early 1990s. The US economy recovered from the recession faster, while Europe faced the ERM crisis in 1992/1993. This created a sizeable economic divergence, which continued until the early 2000s, in part helped by the TMT boom in the US. This period coincided with another large USD bull-rally (1995-02) of more than 30% in the broad real USD index.

The exception to this pattern was in 1994 when the USD was weak vs. G10 countries due to idiosyncratic factors.

And that is helping throw the dollar up against both sterling and the euro, with the dollar index having gained 4.5 per cent since mid-June.

Rate divergence, based on improving data in the US and on the contagion that is forward guidance on the other of the Atlantic, is obviously a very large part of the reason with Nomura’s Jens Nordvig noting that last week “was only the ninth instance of a 30bp+ widening of the 2yr forward short rate spread between the US and Eurozone since the creation of the euro. In addition, the 3-week move of more than 60bp was the second largest since 1999 (only exceeded by a move in 2003)”.

David Woo at Bank of America Merrill Lynch expects the US to keep up its side of the differential bargain (as Asmussen seemed to do the same over here):

But we’d note in the face of seeming consensus that stronger US data doesn’t always lead to a stronger dollar (see 2002-2004 for example), and rate divergences have not always produced tradeable signals. From Nordvig again:

According to Nomura, since 1980, there are only two periods of economic divergence — between the US and Europe and the UK — comparable to what we are observing currently.

The first period was in the early 1980s, when the US unemployment rate peaked in December 1982, but the rate in the UK and Eurozone kept rising beyond this point. This allowed the Fed to start a hiking cycle as early as late-1980, while the BOE was still cutting rates until mid-1981. The impact on the currency market was clear as well, with this helping to exacerbate the broad-based USD rally which continued until the Plaza Accord in 1985. The overall broad USD rally from 1978-85 was more than 50% in real terms.

The second notable divergence was in the early 1990s. The US economy recovered from the recession faster, while Europe faced the ERM crisis in 1992/1993. This created a sizeable economic divergence, which continued until the early 2000s, in part helped by the TMT boom in the US. This period coincided with another large USD bull-rally (1995-02) of more than 30% in the broad real USD index.

The exception to this pattern was in 1994 when the USD was weak vs. G10 countries due to idiosyncratic factors.

Rate divergence, based on improving data in the US and on the contagion that is forward guidance on the other of the Atlantic, is obviously a very large part of the reason with Nomura’s Jens Nordvig noting that last week “was only the ninth instance of a 30bp+ widening of the 2yr forward short rate spread between the US and Eurozone since the creation of the euro. In addition, the 3-week move of more than 60bp was the second largest since 1999 (only exceeded by a move in 2003)”.

David Woo at Bank of America Merrill Lynch expects the US to keep up its side of the differential bargain (as Asmussen seemed to do the same over here):

Even after the biggest Treasury sell-off in years, we fear the balance of risks continues to point to higher Treasury yields: short positioning is still moderate, yields are not yet at levels that would attract long-term value investors (10y Treasury yields one year forward are still only at just 3%!) and outflows from bond funds will likely continue. We have revised up our 10y Treasury yield forecasts to 3% by end- 2013 and 4% by end-2014.

Woo also argues that the negative impact of stronger US growth on the US current account deficit is likely to be more limited than in the past and the positive impact of stronger US growth on the growth of the rest of the world will be also more limited. All of which should make the rates and growth differential between the US and everyone else widen further.

But we’d note in the face of seeming consensus that stronger US data doesn’t always lead to a stronger dollar (see 2002-2004 for example), and rate divergences have not always produced tradeable signals. From Nordvig again:

Figure 1 shows rate spreads vs. EUR; here, the market reverses a decent amount in the four weeks following the divergence in almost all past instances (seven of the past nine). Price action in the currency market is consistent with rates, and EURUSD actually averaged a gain of 1.4% in the following four-week period (see the last row in the table).

A similar theme is seen in GBP as well, where rates reverse the move in about half of the instances analyzed (in the next four weeks), and while GBPUSD does sell off on average, the median move in the currency is not significantly different from zero (not shown in the table).

Really quite hard to look past it all at the same time, though.

A similar theme is seen in GBP as well, where rates reverse the move in about half of the instances analyzed (in the next four weeks), and while GBPUSD does sell off on average, the median move in the currency is not significantly different from zero (not shown in the table).

gipa69

collegio dei patafisici

The WTI carry unwind

Reddit

The fixed income team at Credit Suisse have a good note talking about what’s really driving WTI backwardation. Small hint, they don’t think it’s much to do with Egypt.

They put the backwardation down to three things.

First, there’s genuine seasonal demand for light sweet crude, which is always strongest in the summer months. The trend started at least a month ago.

Second, they believe there is a very strong possibility that a lot of the oil that’s stored at the WTI delivery point at Cushing is not necessarily made up of high-quality, low-sulfur, light crude oil — which is what is being demanded by the market — but of a wider category of oil.

Third, the WTI low-interest rate carry trade is being unwound.

It’s this that’s worth your time:

What happens next will depend on how easy it really is to find a better-yielding cash investment.

It’s also worth thinking about what definancialisation trends will do to those participants that have made a business out of collateralising and financing commodity stores the past few years.

Though, perhaps even higher rates in China will absorb a lot of those commodities from the market, by collateralising them in warehouses — at least until the renminbi stops appreciating against the dollar

The fixed income team at Credit Suisse have a good note talking about what’s really driving WTI backwardation. Small hint, they don’t think it’s much to do with Egypt.

They put the backwardation down to three things.

First, there’s genuine seasonal demand for light sweet crude, which is always strongest in the summer months. The trend started at least a month ago.

Second, they believe there is a very strong possibility that a lot of the oil that’s stored at the WTI delivery point at Cushing is not necessarily made up of high-quality, low-sulfur, light crude oil — which is what is being demanded by the market — but of a wider category of oil.

Third, the WTI low-interest rate carry trade is being unwound.

It’s this that’s worth your time:

Beyond the fundamentals, recent changes in positioning also matter. For the last two to three years, just as the Federal Reserve drove investors to look ever harder for yield, WTI’s steep contango provided a neat carry trade, allowing it to be a fairly steady provider of decent (if unspectacular) returns.

Boiled down to the basics, investors were selling one year out time spreads, where the curve was relatively flat, and waiting for them to move into contango as the futures approached the prompt month, see Exhibit 13. Now that the WTI curve has flipped into backwardation, this trade no longer works and the remaining, perhaps significant, positions are being unwound.

To do so, funds must buy the front and sell the back, further exacerbating WTI’s backwardation.

So, as we’ve noted before, a lot of the US oil that was being pent up in storage to take advantage of positive contango carry, is now likely to be released to the world. The destocking and backwardation is less about a short squeeze and possibly more about there being a sudden cost to hold commodity over cash.Boiled down to the basics, investors were selling one year out time spreads, where the curve was relatively flat, and waiting for them to move into contango as the futures approached the prompt month, see Exhibit 13. Now that the WTI curve has flipped into backwardation, this trade no longer works and the remaining, perhaps significant, positions are being unwound.

To do so, funds must buy the front and sell the back, further exacerbating WTI’s backwardation.

What happens next will depend on how easy it really is to find a better-yielding cash investment.

It’s also worth thinking about what definancialisation trends will do to those participants that have made a business out of collateralising and financing commodity stores the past few years.

Though, perhaps even higher rates in China will absorb a lot of those commodities from the market, by collateralising them in warehouses — at least until the renminbi stops appreciating against the dollar

Similar threads

- Risposte

- 2

- Visite

- 665

Users who are viewing this thread

Total: 1 (members: 0, guests: 1)