Greece is not Argentina

Greece: This Decade's Argentina?

Posted by

Kash | 3/28/2011 07:15:00 PM

There's been a bit of discussion floating around about whether the US's deficit and debt situation makes it appropriate to draw

comparisons with Greece. Of course, such a comparison is ridiculous for a number of reasons, not least because the US has its own currency. But Greece has been on my mind lately for unrelated reasons, including the following news:

Euro economists expect Greek default, BBC survey finds

Greece is likely to default on its sovereign debt, according to the majority of respondents to a BBC World Service survey of European economists. Two-thirds of the 52 respondents forecast a default, but most said the euro would survive in its current form.

...The forecasters the BBC surveyed are experts on the euro area - they are surveyed every three months by the European Central Bank (ECB) - and as well placed as anyone to peer into a rather murky crystal ball and say how they think the crisis might play out. The survey had a total of 38 replies and two messages came across very strongly.

Not only do I agree that default by Greece on its sovereign debt is quite possible... but I think it increasingly likely that policy-makers in Greece may decide that it is the least bad option at this point, particularly in the face of an increasingly hard-line attitude from Germany regarding bailouts (which will only be reinforced by

recent election results).

The problem is easy to lay out: Greece has more debt than it can realistically make payments on, and being a euro country also has a currency over which it has no control. If it had its own currency, it would be in a classic debt crisis similar to several Latin American countries in the 1980s, or possibly Mexico in 1994.

However, it effectively has a fixed exchange rate with the rest of the euro zone, and has invested enormous political and economic capital in maintaining its committment to the euro. In that sense, the best analogy might be with Argentina in 2001, which was struggling to maintain a rock-solid fixed exchange rate with the US dollar through a

currency board arrangement.

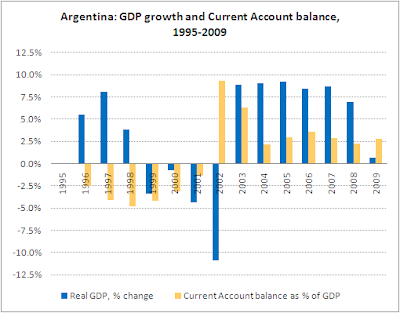

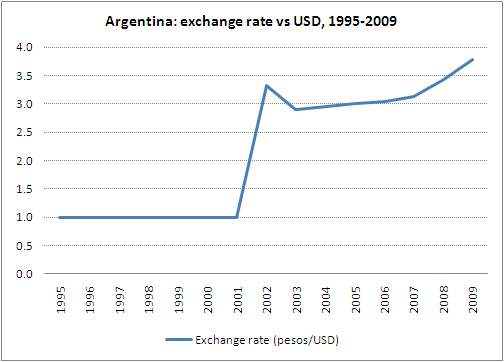

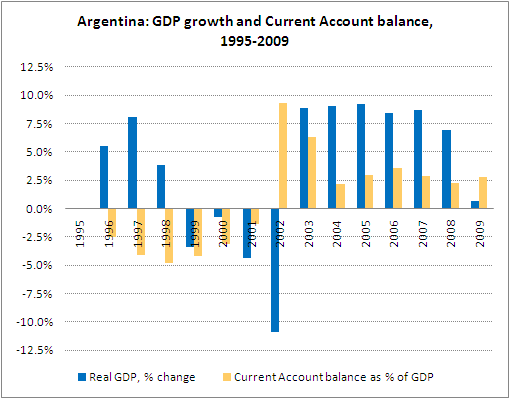

Argentina in the late 1990s had a slowing economy, uncompetitive industries, large current account deficits, and a vast amount of external debt denominated in a currency that was not its own. Sound familiar? In an effort to meet its debt payments while simultaneously keeping its exchange rate pegged to the dollar, the Argentine government squeezed and squeezed the economy. Finally, however, the resulting deflation and recession grew so severe that the government collapsed, and in early 2002 a new government dropped the peg to the dollar (after fiddling with a hybrid system with multiple currencies existing simultaneously) and eventually defaulted on its debt.

And look what happened.

From 1999-2002 Argentina suffered through years of a gradually contracting economy as it tried to maintain its peg with the dollar and service its external debts. When it finally dropped the peg in January of 2002 and then defaulted on its external debts, the economy (along with the value of the peso) crashed quite spectacularly.

But after a year or two, things didn't look so bad in Argentina. And through most of the 2000s, the economy did quite well, despite the loss of the ability to borrow internationally.

I'm not necessarily advocating that Greece follow the same path. However, I do think that the comparison with Argentina in 2001 is a very good one, and because of that, that there is indeed a very good chance that policy-makers in Greece in 2011 will reach the same conclusion that policy-makers in Argentina did in 2002.

Greece is not Argentina

April 2, 2011

I politely disagree with the conclusions of my Angry Bear colleague, Kash, who envisages Greece defaulting in 2011 similarly to Argentina in 2001 (see

AB post here).

I do agree, that the macroeconomic initial conditions in Greece scream default (actually, if you focus just on the measurable factors, like the current account, debt levels, or fiscal imbalances, Greece is much worse than Argentina in 2001 –

see Table 4 of this IMF paper to see Argentina’s initial conditions and compare them to Greece in 2009 using the

IMF World Economic Outlook Database).

Where I disagree, arguing that Greece is not like Argentina, is that the debt crisis in Argentina didn’t bring down the banking system of Latin America overall. In contrast, the default of Greece has the potential to do just that in Europe.

In Argentina, the Latin American banking system (and sovereign bonds, for that matter) was quite resilient in the face of the sovereign default in Argentina. Uruguay was the exception, whose two largest private banks, Banco Galicia Uruguay(BGU) and Banco Comercial (BC), which account for 20% of the country’s total, saw near-term liquidity pressure and an ensuing banking crisis in 2002 (see this

IMF paper for a history of banking crises). All else equal, the IMF reports

only minor impact to the region as a whole:

With the possible exception of Uruguay, economic and financial spillovers from the Argentine crisis appear to have been generally limited to date—as indicated, for example, by the muted reactions of bond spreads in most other regional economies and their declining correlation with those of Argentina, together with other favorable trends in financial market access and the general stability of exchange rates over recent months.

In contrast, the European banking system is highly interconnected. For example, according to the

German Bundesbank, Germany’s bank exposure to Spain was roughly 136 bn euro in December 2010, where most of it is held in the form of Spanish bank paper, 56.4 bn euro, and Spanish enterprises, 58.3 bn euro; the rest is in sovereign debt. Furthermore, German banks are sitting atop 25 bn euro in (worthless) Greek paper, primarily in the form of sovereign debt. Euro area countries are exposed to other banks AND the sovereign; but more importantly, the ones that save (run current account surpluses) are the ones holding the worthless (in some cases) bank and government debt. (read more after the jump)

Bank risk is a big risk in Europe. Based on the consolidated banking data at the

Bank for International Settlements (BIS) data, German banks hold 22% of the Greek external debt load i.e., bank debt + sovereign debt + corporate debt), while French banks hold 32% (see Tables below). Furthermore, German banks are sitting on 20% of all Irish external debt, 14% of Italy’s, and 21% of Spain’s external debt load.

So the question is, not what will happen if Greece defaults, per se; but will a Greek default set off a chain reaction liquidity crunch that challenges asset valuations in the other Euro area banking systems (for bank paper and sovereign paper)? I suspect that it will, since the European banks are still building their capital buffers.

My point is, the Germans are partial to NOT letting Greece default. All fiscal austerity aside, the Germans have demonstrated that they’d rather write a check than take the writedowns, at this time. Therefore, from this perspective, I find it very unlikely that Greece defaults this year (or next, really).

Now, you’re probably thinking: well, it’s in Greece’s best interest to default. Willem Buiter calls

Greece leaving the Euro area ‘irrational’. An irrational chain of events must be put in place in order to go presage such a disorderly default (see

8. ‘Break-Up Scenarios for the euro area’ in the publication)

BIS data representation I: in Shares of external debt outstanding (click to enlarge)

BIS data representation II: in levels of external debt outstanding (click to enlarge)

Rebecca Wilder

Greece is not Argentina | AthensWire

Fare i complimenti a Tommy per le sue analisi culturali, storiche ed economiche comincia ad essere ripetitivo

Fare i complimenti a Tommy per le sue analisi culturali, storiche ed economiche comincia ad essere ripetitivo ") .

.