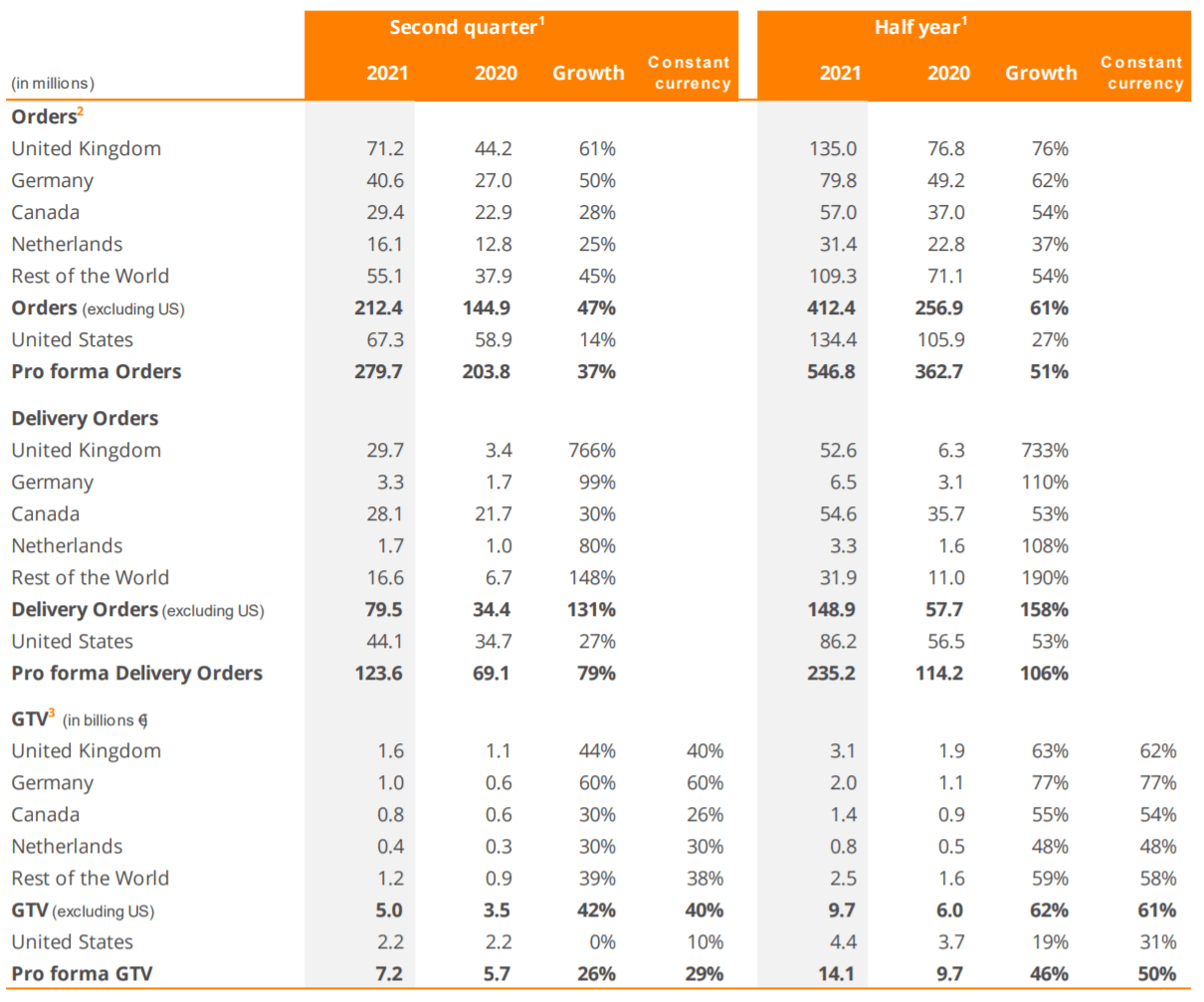

At first glance JET's results seemed magnificent with order growth higher than expected across most markets. When diving deeper into the numbers it is clear that the order growth of the marketplace disappoints across most markets; for example, in the United Kingdom, marketplace orders grew by approximately 0% YoY. Delivery orders have risen at tremendous rates; unfortunately, these orders are loss-making in the short term.

The FY 2021 order growth guidance excluding Grubhub has also been raised to >45% reflecting the strong growth in delivery orders. Especially in the UK management clearly focuses on market share over profitability. And believes that the

best food delivery marketplace will eventually acquire high returns on invested capital.

The effect on EBITDA margins is clear: the company is guiding for adjusted EBITDA margins of -1% to -1.5% of the gross merchandise value. That implies an adjusted EBITDA of €-280 to €-450 million. This guidance is far worse than consensus estimates and has led to a severe de-rating of the stock.

(Source: Just Eat Takeaway IR)

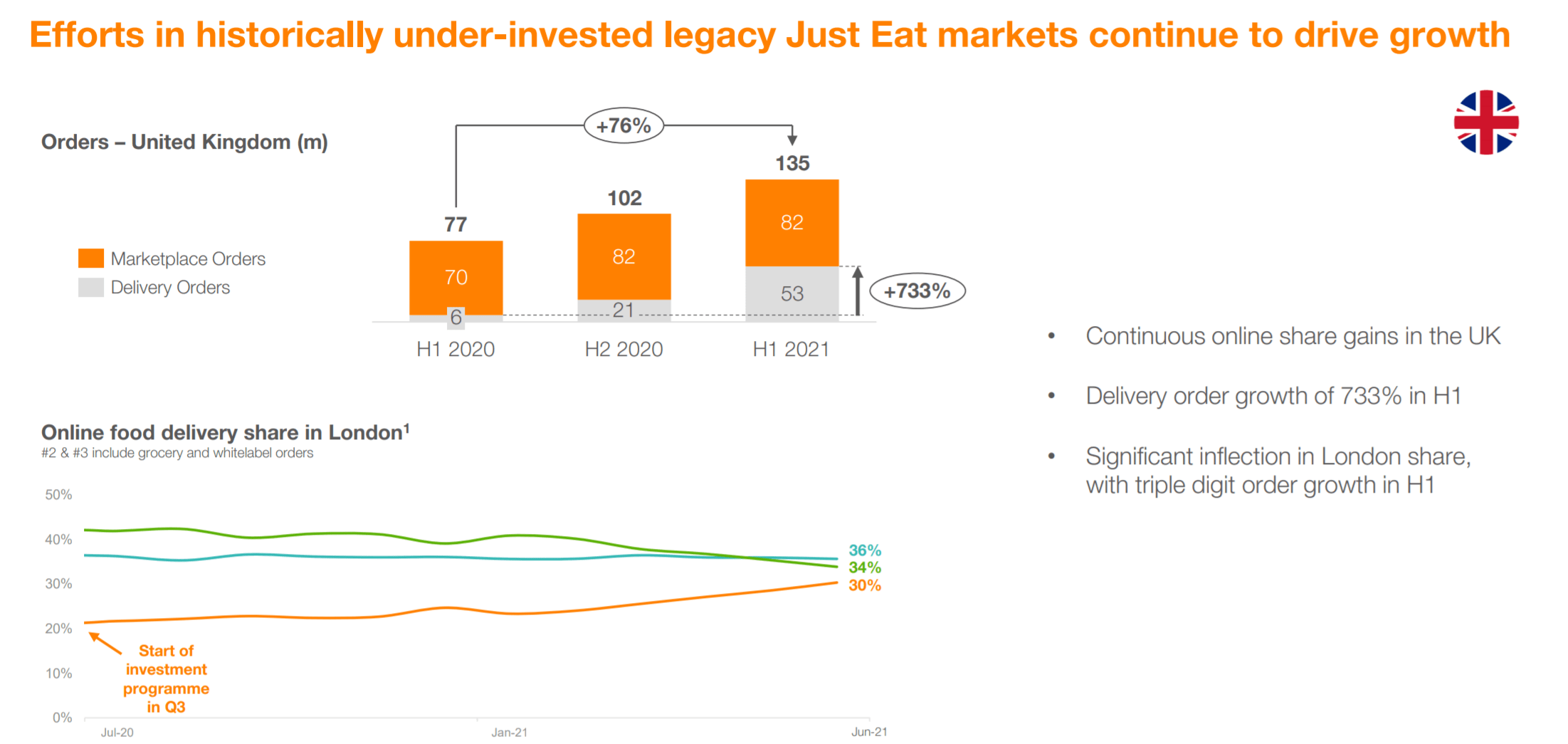

JET is mainly focusing on expanding its

moat in the United Kingdom. Here competition is fierce and management has made it its public goal to 'conquer the UK'.

Just Eat already is the market leader outside of London, and is closing the gap to competitors in terms of market share and restaurant selection in London. The biggest problem is Deliveroo (

OTCPK ROOF

ROOF); while Just Eat grew its market share by 50% during the last six months in London Deliveroo did not lose share. I believe this is caused by multiple reasons.

First, Deliveroo's

Signature is a white-label service; this service does not strengthen the network effects of Deliveroo. Deliveroo only performs the delivery but the food is ordered through third-party apps: it adds market share but does not add network effects. This white label service probably experienced hefty growth. And Deliveroo has experienced growth in groceries which is a different market than food delivery.

Considering these trends and deducting these growth drivers from Deliveroo's market share, then Just Eat grew its food delivery market share at a rapid pace relative to all competitors in London.

I also note that JET is guiding for 45%+ H2 2021 order growth and Deliveroo for 15-32% H2 2021 order growth. Clearly implying JET will continue taking market share.

(Source: Just Eat Takeaway IR)

The profitability dilemma

A couple of weeks ago Deliveroo announced results: they experienced higher than expected order growth but profitability was worse than expected. This led to a significant rise in the stock price. Yet when Takeaway blows apart growth expectations this leads to a de-rating of the stock. What worries the market?

The main concern is probably the inferior unit economics of Takeaway versus competitors. By employing its couriers and providing minimum-wage guarantees, sick pay etc.; instead of employing its couriers using a freelance model the company's cost per delivery is higher. This makes growth more expensive.

The market is pessimistic about the long-term profitability of logistical orders. But the facts point to something else. Italy and Spain have already passed laws to make it compulsory for food delivery platforms to hire their drivers.

It seems plausible as the power of platforms and tech companies grow; governments will put more effort into defending workers' rights. If that is the case JET is making an adequate decision by utilizing a labor model that is future proof. If that is not the case the company will burn a significant amount of capital by operating an inferior labor model.

Takeaway.com is struggling with a profitability dilemma, very similar to the innovator's dilemma seen with disruptive technologies. Long-term logistical orders will probably make up a big portion of all food delivery orders, and in the long term, these orders will strengthen the moat of the company, increase GMV and increase profits. But short-term logistical orders actually significantly lower profitability; which make it seem as if these orders are destroying value.

I believe the recent stock's fall is due to the fear of logistics orders cannibalizing the more profitable marketplace orders. I believe this fear is overdone. In reality, most logistical orders are from newly signed up dine-in restaurants that probably have a smaller focus on takeaway services. Large takeaway restaurants will probably continue to employ their own drivers. If that is the case JET is significantly undervalued. I believe these logistical orders will defend the marketplace orders - so the logistical network makes the marketplace more valuable and harder to disrupt.

This is JET's core philosophy. With the logistical network, people stay on JET's platforms to order McDonald's (NYSE:MCD) in addition to ordering food from JET's marketplace restaurants. The order frequency goes up. This is the superior hybrid model I discussed previously. But the market is pessimistic and does not believe the hybrid model will work.

I also note that as penetration in the market grows and growth rates decline profit pools become easier to defend; the so-called moat becomes stronger and stronger. That is why I expect high returns on invested capital in the long-term for this company.

Valuation

A short reminder of Takeaway's low valuation. Market cap is €14.27 billion, enterprise value €11 billion when deducting the iFood stake. If you assume €2 billion in gross profits for 2021 - which indicates a gross profit of margin of GMV around 6.7% - the company would be selling at a forward 5.5 EV/gross profit, very cheap for a company growing so fast.

Takeaway

Management focuses on market share over short-term profitability for the long-term success of the enterprise and operates a delivery model that in the short-term has inferior unit economics to the freelance model but in the long-term is more durable.

Why? Most members of the management team have a very large portion of their wealth invested in this company. They do not care about short-term market sentiment but long-term value creation and they believe this strategy maximizes long-term value creation.