Son bravi a far finta di niente. Qui a San Francisco da "uomo della strada" la crisi USA e della California in particolare non la percepisco assolutamente.

")

nessun problema in California

1.8 Million California Mortgages Underwater. In 2008 100,000 Renters were added. 2010 California Housing Market Trends. How Banks Hoodwinked the Public into Believing the Bailouts were to help the Housing Market.

1.8 Million California Mortgages Underwater. In 2008 100,000 Renters were added. 2010 California Housing Market Trends. How Banks Hoodwinked the Public into Believing the Bailouts were to help the Housing Market.

As we wind the year down the California housing market is entering a new chapter in its bubble saga. 2009 brought many new factors to consider in how the housing correction will play out. One major trend was the growing number of moratoriums. These programs largely failed at preventing foreclosure and only pushed the inevitable down the road creating a cryogenic toxic mortgage. The growing number of

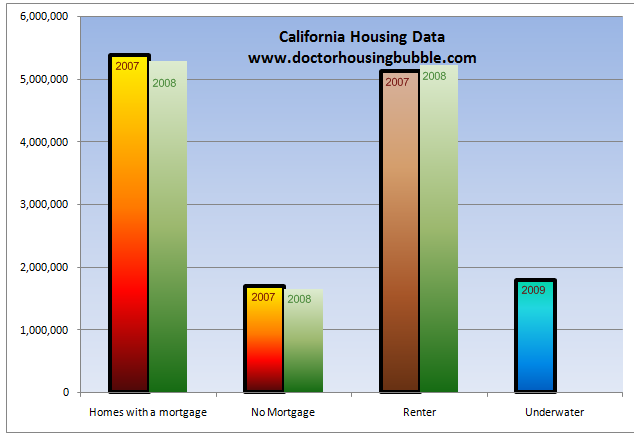

shadow inventory has been mounting as well. A few articles appeared in the L.A. Times and O.C. Register discussing this topic. Hopefully we’ll see some opinion pieces discussing how shady bank practices are when banks claim housing numbers look good when they know that the numbers on the books state otherwise. As of today, on the eve of a new year, roughly 1,800,000 mortgages in California sit underwater. That is, the home backing the mortgage is not even worth the current balance.

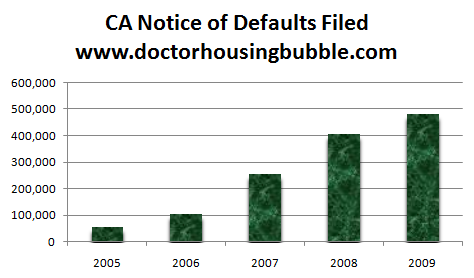

This is hard for people to imagine. Recent annual data from 2008 showed that California added 100,000+ new renters in 2008. When the 2009 data is released late in 2010 we should expect a similar trend. 2009 saw a record number of notice of defaults filed:

So 2009 was the worst year for California housing if we consider people not paying their mortgage as a significant criteria. And the above chart is largely responsible for the growing number of

shadow inventory. In a typical foreclosure process, after a notice of default is filed a home will be taken back in 3 to 6 months. Take for example the 135,000 notice of defaults filed in Q1 of 2009. With a cure rate of 3 to 5 percent according to recent reports we would expect 128,000+ of these homes to be taken back in Q3 of 2009 by the bank. How many foreclosures occurred? 50,000. Now this isn’t a new trend or something that is shocking. In fact, with the

HAMP initiative it has become a formalized process. Yet HAMP has only converted some 4 percent of trial modifications to permanent status (they have extended the deadline to the end of January as if this was going to miraculously boost the numbers). Plus, we have yet to see drilled down statewide data. California also has toxic mortgages like

option ARMs and Alt-A products that largely do not qualify for HAMP. Many of the option ARMs recast in 2010.

But let us look at the overall California market:

California has an extremely large renting population. In 2008 we saw a massive shift of 100,000 additional renters. This number almost perfectly correlates with the 91,000+ drop of homes with a mortgage. In 2008 California had almost the same number of renters as homeowners with a mortgage. It is a safe bet that in 2009 we have more renters than homeowners with a mortgage. I hesitate to call someone with massive negative equity a homeowner. Of those with a mortgage, nearly 2 million owe more than what their home is worth. They are worse off than a renter.

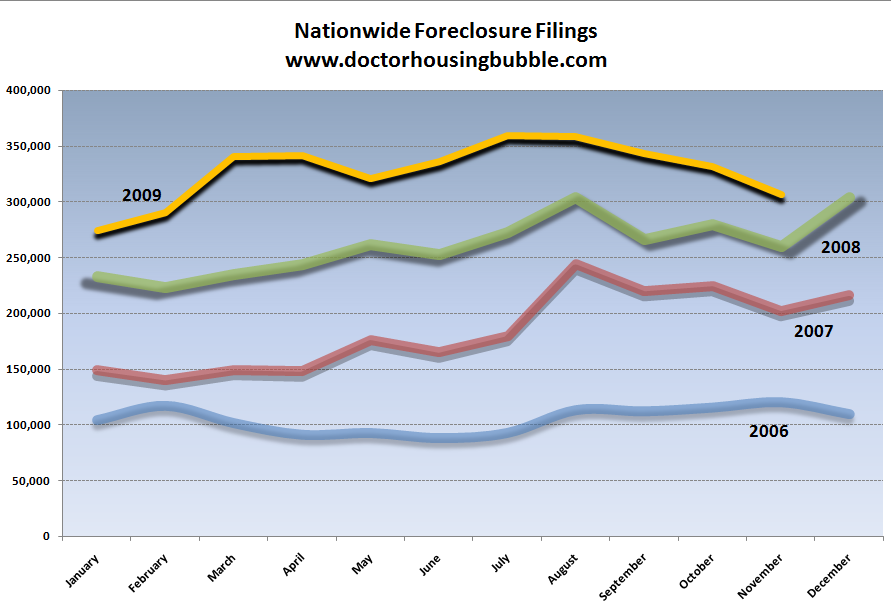

Banks have been playing this absurd game with taxpayer money. Since the recession started we have seen trillions of banking subsidies and direct bailouts. Yet here we are with foreclosures still near their peak and the economy still in the dumps:

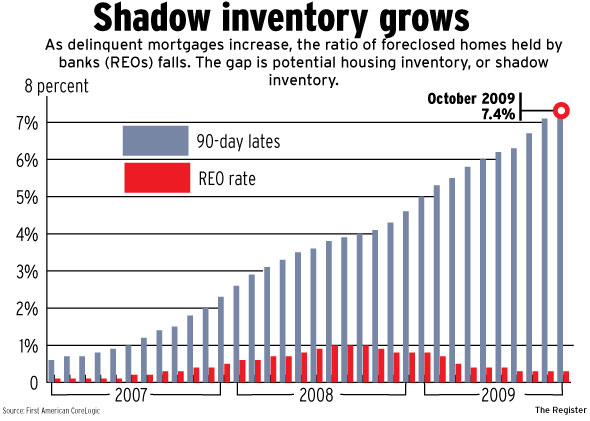

Matthew Padilla at the

O.C. Register has a chart showing the growth of the shadow inventory:

Source:

OC Register

So what are we looking at above? While foreclosures in Orange County have been steadily dropping loans that are 90+ days late are now at a record high! In other words, banks have been covering up their eyes and pretending everything is okay. This is the nonsense that is called a “solution” to the current problem. If ignoring a serious issue like this is good news then a gambler should keep on gambling even if he is in the hole for millions. This is the

shadow inventory. We have never been in a situation like this. It is the height of stupidity to give banks the authority to resolve this mess when they are largely the culprits of bringing down our economy. With the trillions banks have received we could have paid off every single mortgage in the U.S. But as you have figured out by now the bailouts were never about helping the public. The bailouts were to protect the

entrenched crony interests of Wall Street.

It is amazing that government policy is only now starting to connect the fact that the employment situation is so dismal and that may be a reason for the continued problems with housing. I tend to believe that D.C. and Wall Street are now one in the same so they already knew this and sold the bailouts as assistance for the people. That has been a major sham. Early reports on HAMP show that the process is laborious and painstaking for those trying to get a modification. You mean the same people that made $500,000 mortgages with your cat as a co-signer in 24 hours are no longer able to rush through paperwork? The banks are largely lagging because they already have taxpayer money so what is the big rush? They can simply go back to gambling on Wall Street while the real economy looks like this:

The California unemployment rate went from 8.7 percent in December of 2008 to 12.3 percent today. Without a doubt this has something to do with the 90+ days late jumping off the charts. What use is modifying a mortgage if you have no job? Yet this has been the tunnel vision policy of our government since December of 2007 and we continue to allow Wall Street to write the path forward. The PR machine is going heavy that things are now dandy because the stock market is up 60+ percent but the reality is much different. Foreclosures are still sky high and hiring is still anemic.

Is it any wonder why so many loans are underwater in California? Maybe the market is trying to say something that prices are still too high given the current economy of the state. We are going to start the year off with a $21 billion budget deficit. How is this good for housing but more importantly the economy? Banks will continue to rip people off and drain taxpayer money because nothing has come in the way of solid reform. There is a commission that is finally going to look into the causes of this crisis but findings won’t be out until late in 2010! First, banks and Wall Street are the primary causes of this crisis thanks to their bedfellow the

Federal Reserve which serves as a pseudo-government agency to funnel money into the banking and financial sector. Alan Greenspan dropping rates to 1 percent juiced the housing market completely. Would people be buying homes if mortgages were 10 percent? They’d think twice. Plus, the easy interest free money was more a gift to Wall Street to gamble in the global stock markets. One argument goes “well people should know better than to borrow $500,000 from a bank.” Poor bank. How about we only allow the bank to lend their money and let us see if they still make those loans with zero government backing. Something tells me lending standards would change overnight.

Are people to blame as well? Absolutely. But many are paying the price with job losses and foreclosures. They are taking their knocks. Yet Wall Street has siphoned off every penny from the taxpayer to ensure that they don’t lose any money in this downturn. They talk about moral hazard when it comes to the public but when it comes time for their punishment they like to pull the hypocrite card out.

And things are going so good that

Fannie Mae and Freddie Mac are having their caps pushed upwards. Turns out losses are just pouring in. Do you remember the gall of these people telling us we were somehow going to turn a profit on this? This was the ultimate sucker play. If banks had to make mortgages with their own money you can rest assured the interest rate would be somewhere between 8 and 10 percent and they would be limiting who they lend money too (I would assume a more sizeable down payment as well). But instead, banks with their horrible underwriting standards are actually dishing out government backed loans with artificially low rates. These are the loans that are now imploding. Banks don’t give a crap since they don’t hold the note. So if this is the case, why do we even need the bank? Why not have the government make the loan directly to the public? Because banks want to suck every nickel out of your wallet.

So until we get any real reform we can expect to live in a 1984 like world where we hear propaganda that the economy is fine and housing is recovering. Don’t worry, after all banks were in charge this decade and look how well things went.

")