Greek Bailout

Europe's leaders came up with a new plan to contain the debt crisis and rescue the peripheral economies.

Though not all of the details of this plan are known, here is a rough summary: Greece is being offered an additional 150 billion Euros of direct and indirect aid.

The direct aid comes in the form of new financing from the EU and the IMF, to the tune of 109 billion Euros. These loans will have long maturities (30 years) and low interest rate (around 3.5%). The rest of the aid comes from the private sector. Financial institutions have

agreed to reduce the value of Greek debt they hold by roughly 20%, something which analysts believe will not significantly affect their share price, as the market has already factored in such a scenario.

This will happen through a swap - bond holders will exchange the debt they own with new bonds of longer maturities and lower rates

. However, these new bonds will be rated AAA and backed by the EU. There are two additional interesting points here: the European Central Bank (ECB) has declared that it will continue accepting Greek bonds, even if Greece is officially termed 'Defaulted' by the rating agencies, as collateral;

and the International Swaps & Derivatives Association (ISDA) has stated that the plan outlined will not trigger an activation of CDS contracts even though Greece may officially be in default, as private participation to the programme is 'voluntary'. In my view, this is quite unfair, but this is a separate discussion.

So far, I have focused on the plan's provisions for Greece. However, EU leaders also agreed to extend the EFSF's power and size, so that it can intervene in the capital markets to purchase bonds of EU economies if they come under pressure. Furthermore, the EFSF will have the right to recapitalise illiquid banks in the EU.

Now, there are a few questions that need to be answered:

- Does it really make sense for Greece to be borrowing from the EFSF at 3.5% interest, when France can only borrow at 3.8%?

- As

zero-hedge points out, the EFSF has a 20% collateral guarantee rule. Furthermore, analysis by the research firm Bernstein notes that for EU to remain stable, the EFSF should cover Belgium and Italy in addition to the other peripheral economies. Hence, the fund should grow to at least 1.4 trillion Euros. How will Germans feel when they found out that their share to this fund amounts to 790 Billion Euros?

- Finally, is this solution really a help to Greece? Having spoken to a few friends back home, the answer I got is 'it depends on which channel you follow'.

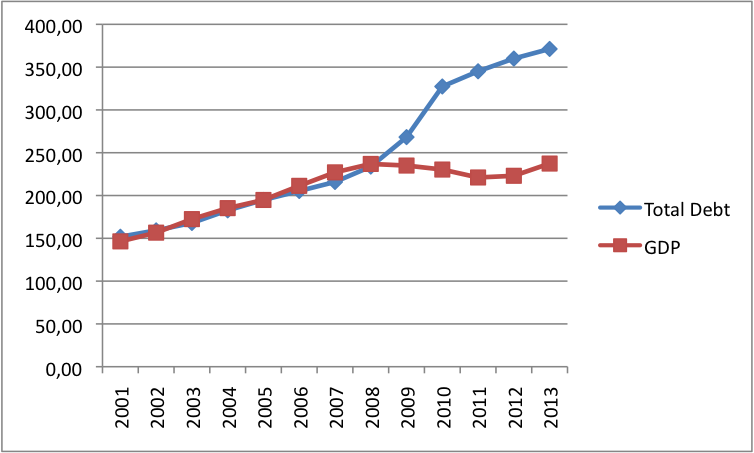

The fact of the matter is that Greece's debt as a percentage of GDP will remain very high, and there is no indication that it's GDP growth will pick up in the future.

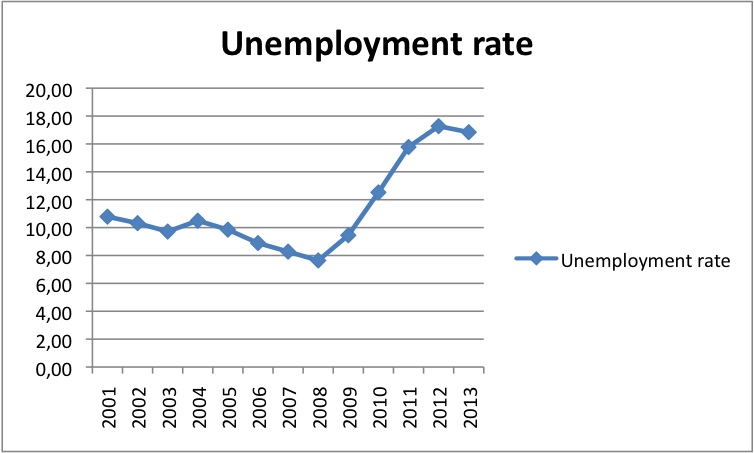

In fact, all the macro trends paint a bleak image of the future. The unemployment rate is very high, and projected to grow even more.

It is not forecasted to drop under 14% until at least 2016 (the source for this, and for these charts is

Global insight).

Moreover, household consumption has decreased, as people prefer to save rather than spend. This, naturally, will have an impact on Greek businesses.

Finally, another worrying trend is emigration, as more and more people choose to study or work abroad. As I've mentioned in other posts, Greece is being drained of its talent.

Given all of these statistics, why did the share price of Greek companies, and especially banks skyrocket by more than 7% during Friday's trading session? There is clearly a wave of misguided optimism in the market, and this cannot end well.

Is there really a way out for Greece? To quote [ame="http://www.youtube.com/watch?v=GTQnarzmTOc"]a great Econstories video[/ame], "the economy is not a class you can master in college - to think otherwise is the pretense of knowledge"; I cannot predict the future, and I do not profess to be able to forecast the effects of this bail out deal.

One thing I can say though is that

Greece has ways to boost its economy. It needs to attract investment and support its talent. The way to do this is to eliminate bureaucracy and shape a culture than encourages entrepreneurship. There's no reason why Greece couldn't have its own Silicon Valley. In fact, I believe that if things go well, there might be a large market for venture capital in Greece. But this is only if entrepreneurs no longer need a thousand signatures to establish a company.

") .

.

.

.