Stai usando un browser molto obsoleto. Puoi incorrere in problemi di visualizzazione di questo e altri siti oltre che in problemi di sicurezza. .

Dovresti aggiornarlo oppure usarne uno alternativo, moderno e sicuro.

Dovresti aggiornarlo oppure usarne uno alternativo, moderno e sicuro.

NicOx.... in attesa di.....

- Creatore Discussione DickSIM

- Data di Inizio

viralic

Forumer storico

E finalmente anche l'AC170 è stato ridepositato; ora al massimo tra 6 mesi avremo il verdetto della FDA. Nel frattempo credo che concluderanno l'accordo con chi venderà negli USA il Zerviate.

Piano, piano le cose vanno avanti. Chissà che sia davvero l'anno buono ?

Entro 8 aprile sapremo se FDA approverà entro 2 mesi o entro 6 mesi Zerviate.

Aeiou

▲ + 444%

Non pensavo a questo mi riferivo al fatto che Valeant sta vendendo il vendibile: "Re-acquisition of all commercial rights to sell RUCONEST® in North America from Valeant in December 2016 in a deal valued at $125 million."Ciao Aeiou, per noi la situazione è più complessa dato che i diritti del Vyzulta sono di Bausch + Lomb. Non penso che molleranno tanto facilmente una gallina dalle uova d'oro come il Vyzulta.

viralic

Forumer storico

Non pensavo a questo mi riferivo al fatto che Valeant sta vendendo il vendibile: "Re-acquisition of all commercial rights to sell RUCONEST® in North America from Valeant in December 2016 in a deal valued at $125 million."

se Valeant dovesse decidere di vendere B+L , allora il Vyzulta andrebbe alla nuova proprietà. Nicox non può ricomprare i diritti. e fare un nuovo accordo......Il Vyzulta si vende con B+L , oppure valeant preferirà vendere altre cose e tenersi uno dei suoi gioielli più redditizi.

viralic

Forumer storico

Interessante articolo su SEEKING ALPHA

Why Valeant's Bausch & Lomb Is Worth More Than You Might Think

Mar. 10, 2017 4:58 PM ET

|

| About: Valeant Pharmaceuticals International, Inc. (VRX)

by: Arjan Sharma

Arjan Sharma

Value, special situations, growth

Summary

87% of Bausch & Lomb EBITDA is independent of US prescription pricing model.

New marketing campaigns are targeting Chinese and Japanese growth.

Vyzulta (Vesneo) FDA approval is likely for Q2 2017.

Worldwide eye care market is growing at a rapid pace.

By 2020 Bausch & Lomb will be worth more than the cumulative debt of Valeant.

Bausch & Lomb is a division of Valeant Pharmaceuticals International, Inc. (NYSE: VRX) and is one of the best-known and most respected healthcare brands in the world. The company offers a wide range of eye health products including, contact lenses, drops, pharmaceuticals, and eye surgery products.

Bausch & Lomb is seen as Valeant's "crown jewel" investment, there are many articles on Seeking Alpha trying to provide a fair market value for Bausch & Lomb with varied depth in analysis. This article will examine the Bausch & Lomb business as well as trends in the eyecare market to determine a fair market value for Bausch & Lomb.

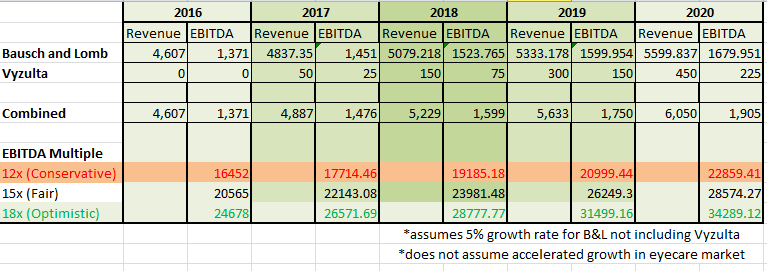

In 2016 Bausch & Lomb achieved revenues of $4.6 Billion and an EBITDA of ~$1.3 Billion. The overall revenues increased year over year, however, due to many management problems at Valeant the overall bottom line earnings decreased by about 14%. Conservative estimates from Valeant suggest that Bausch & Lomb should experience 4-6% yearly growth in 2017-2020.

In Valeant's presentation on January 10th, 2017 at the JP Morgan Healthcare Conference, CEO Joseph Papa discussed some initiatives currently underway to grow the Bausch & Lomb Business.

The Chinese and Japanese markets reflect a huge growth opportunity for the Bausch & Lomb franchise. Valeant is currently taking strategic marketing approaches in both countries to continue to build and grow on the success of the Bausch & Lomb Brand.

By gaining distribution at a top pharmacy chain and increasing the e-commerce business Bausch & Lomb should be able to easily achieve the 4-6% growth number just by seeing substantial growth in these two regions.

Newly elected president Donald Trump has mentioned on numerous occasions that he intends to implement new policy and competition to the prescription drug market. Whether this initiative is successful or not, there has been pressure on the pharmaceutical industry when it comes to pricing. With Bausch & Lomb, ~87% of EBITDA is independent of the US prescription pricing model. This suggests that any valuation for Bausch & Lomb should not be similar to the pharmaceutical sector in the US, however more similar to large international consumer goods (in terms of EBITDA multiples).

Potential buyers (or shareholders in the event of a spin off) should consider that Bausch & Lomb is a stable asset that will not face any pressure from US prescription pricing.

A new drug Vyzulta (previously known as Vesneo) a (latanoprostene bunod ophthalmic solution) used to treat patients with Glaucoma or Ocular Hypertension is also set to be approved by the FDA by Q2 2017. Vyzulta will use the strong branding of the Bausch & Lomb franchise in eye care as a first-to-enter drug to tackle this niche market. The projected market sizes for Glaucoma is $3 billion annually and ~$1.6 billion for ocular hypertension (according to Valeant's Q1 result presentation).

Assuming no growth in these market sizes (which is irrationally conservative with the aging population, reliance on screens, phones etc. this will be further discussed later in the article) Vyzulta should capture a market share of at least $1 billion/year. Valeant management indicated that drugs that were not yet approved were not included in guidance numbers for 2017 and onwards. This suggests that the approval of Vyzulta will further increase the growth expectations from Bausch & Lomb.

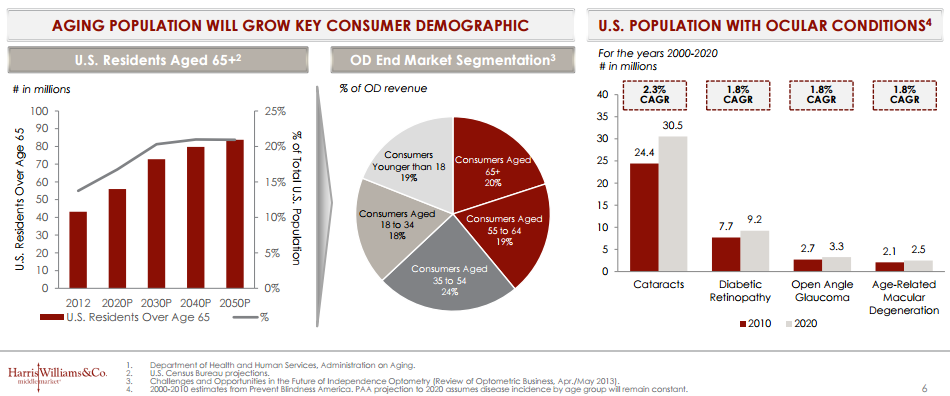

Vision and eye care is seen to be growing at above industry averages due to increased reliance on screens and a rapidly aging population. Research shows that both the aging population and population with ocular conditions in the US is expected to grow until 2050.

A study published in 2014 titled "Global prevalence of glaucoma and projections of glaucoma burden through 2040: a systematic review and meta-analysis." suggests that the population with glaucoma worldwide will increase to over 111.8 million by 2040, with a disproportionate growth seen in people residing in Asia and Africa.

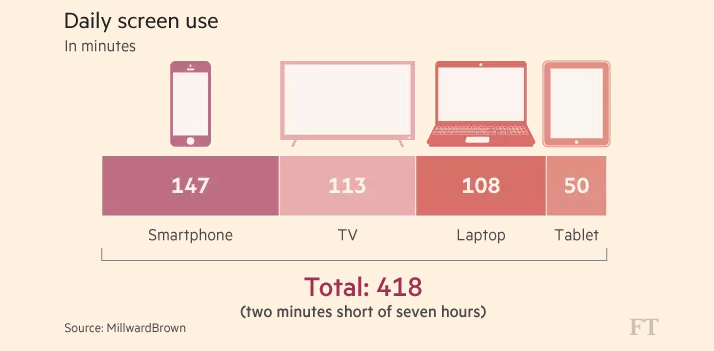

Further, there is new research by MillwardBrown that shows that globally a 16-45 year old typically spends 418 minutes per day look at screens.

Though this area of research is fairly new, there are already trends showing that using screens before bed upset the release of melatonin, adversely impacting our bodies sleep schedule. Initial studies also suggest that there is an increased level of myopia (nearsightedness) in children, research from the UK College of Optometrists shows that nearly 16.4% of UK children are myopic, compared with 7.2% in the 1960's.

Looking at screens can also increase eyestrain, eye fatigue, and dry eyes for individuals. As there is more research done on the impact of screen usage in our lifestyle, there will likely be an increased correlation between screen time and eye health.

It is critical that Bausch & Lomb meet projected growth numbers over the next few years to ease concerns about the deterioration of the business. If the downtrend seen in 2016 continues, this will severely impact the valuation of the business and result in both lower EBITDA for Valeant as well as a lower EBITDA multiple for market value analysis.

Conclusion

With the worldwide eye care market growing rapidly, and Bausch & Lombs strong brand presence worldwide. The asset in 2020 is likely to be worth more than the total amount of debt owed by Valeant at that time (assuming total debt for Valeant is $22 billion by 2020).

Currently, the asset of Bausch & Lomb is experiencing depressed valuation due to challenges at Valeant. As these challenges are overcome and Bausch & Lomb continues its worldwide growth, it will be a very attractive asset to Valeant or others. A potential strategy for Valeant would be to spin-off a small percentage (20%-30%) of Bausch & Lomb via IPO and maintain control of the asset.

Disclosure: I am/we are long VRX.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

About this article:

Expand

Author payment: $35 + $0.01/page view. Authors of PRO articles receive a minimum guaranteed payment of $150-500. Become a contributor »

Tagged: Investing Ideas, Long Ideas, Healthcare, Drug Delivery & Accessories, Canada

Problem with this article? Please tell us. Disagree with this article? Submit your own.

T

Why Valeant's Bausch & Lomb Is Worth More Than You Might Think

Mar. 10, 2017 4:58 PM ET

|

| About: Valeant Pharmaceuticals International, Inc. (VRX)

by: Arjan Sharma

Arjan Sharma

Value, special situations, growth

Summary

87% of Bausch & Lomb EBITDA is independent of US prescription pricing model.

New marketing campaigns are targeting Chinese and Japanese growth.

Vyzulta (Vesneo) FDA approval is likely for Q2 2017.

Worldwide eye care market is growing at a rapid pace.

By 2020 Bausch & Lomb will be worth more than the cumulative debt of Valeant.

Bausch & Lomb is a division of Valeant Pharmaceuticals International, Inc. (NYSE: VRX) and is one of the best-known and most respected healthcare brands in the world. The company offers a wide range of eye health products including, contact lenses, drops, pharmaceuticals, and eye surgery products.

Bausch & Lomb is seen as Valeant's "crown jewel" investment, there are many articles on Seeking Alpha trying to provide a fair market value for Bausch & Lomb with varied depth in analysis. This article will examine the Bausch & Lomb business as well as trends in the eyecare market to determine a fair market value for Bausch & Lomb.

In 2016 Bausch & Lomb achieved revenues of $4.6 Billion and an EBITDA of ~$1.3 Billion. The overall revenues increased year over year, however, due to many management problems at Valeant the overall bottom line earnings decreased by about 14%. Conservative estimates from Valeant suggest that Bausch & Lomb should experience 4-6% yearly growth in 2017-2020.

In Valeant's presentation on January 10th, 2017 at the JP Morgan Healthcare Conference, CEO Joseph Papa discussed some initiatives currently underway to grow the Bausch & Lomb Business.

The Chinese and Japanese markets reflect a huge growth opportunity for the Bausch & Lomb franchise. Valeant is currently taking strategic marketing approaches in both countries to continue to build and grow on the success of the Bausch & Lomb Brand.

By gaining distribution at a top pharmacy chain and increasing the e-commerce business Bausch & Lomb should be able to easily achieve the 4-6% growth number just by seeing substantial growth in these two regions.

Newly elected president Donald Trump has mentioned on numerous occasions that he intends to implement new policy and competition to the prescription drug market. Whether this initiative is successful or not, there has been pressure on the pharmaceutical industry when it comes to pricing. With Bausch & Lomb, ~87% of EBITDA is independent of the US prescription pricing model. This suggests that any valuation for Bausch & Lomb should not be similar to the pharmaceutical sector in the US, however more similar to large international consumer goods (in terms of EBITDA multiples).

Potential buyers (or shareholders in the event of a spin off) should consider that Bausch & Lomb is a stable asset that will not face any pressure from US prescription pricing.

A new drug Vyzulta (previously known as Vesneo) a (latanoprostene bunod ophthalmic solution) used to treat patients with Glaucoma or Ocular Hypertension is also set to be approved by the FDA by Q2 2017. Vyzulta will use the strong branding of the Bausch & Lomb franchise in eye care as a first-to-enter drug to tackle this niche market. The projected market sizes for Glaucoma is $3 billion annually and ~$1.6 billion for ocular hypertension (according to Valeant's Q1 result presentation).

Assuming no growth in these market sizes (which is irrationally conservative with the aging population, reliance on screens, phones etc. this will be further discussed later in the article) Vyzulta should capture a market share of at least $1 billion/year. Valeant management indicated that drugs that were not yet approved were not included in guidance numbers for 2017 and onwards. This suggests that the approval of Vyzulta will further increase the growth expectations from Bausch & Lomb.

Vision and eye care is seen to be growing at above industry averages due to increased reliance on screens and a rapidly aging population. Research shows that both the aging population and population with ocular conditions in the US is expected to grow until 2050.

A study published in 2014 titled "Global prevalence of glaucoma and projections of glaucoma burden through 2040: a systematic review and meta-analysis." suggests that the population with glaucoma worldwide will increase to over 111.8 million by 2040, with a disproportionate growth seen in people residing in Asia and Africa.

Further, there is new research by MillwardBrown that shows that globally a 16-45 year old typically spends 418 minutes per day look at screens.

Though this area of research is fairly new, there are already trends showing that using screens before bed upset the release of melatonin, adversely impacting our bodies sleep schedule. Initial studies also suggest that there is an increased level of myopia (nearsightedness) in children, research from the UK College of Optometrists shows that nearly 16.4% of UK children are myopic, compared with 7.2% in the 1960's.

Looking at screens can also increase eyestrain, eye fatigue, and dry eyes for individuals. As there is more research done on the impact of screen usage in our lifestyle, there will likely be an increased correlation between screen time and eye health.

It is critical that Bausch & Lomb meet projected growth numbers over the next few years to ease concerns about the deterioration of the business. If the downtrend seen in 2016 continues, this will severely impact the valuation of the business and result in both lower EBITDA for Valeant as well as a lower EBITDA multiple for market value analysis.

Conclusion

With the worldwide eye care market growing rapidly, and Bausch & Lombs strong brand presence worldwide. The asset in 2020 is likely to be worth more than the total amount of debt owed by Valeant at that time (assuming total debt for Valeant is $22 billion by 2020).

Currently, the asset of Bausch & Lomb is experiencing depressed valuation due to challenges at Valeant. As these challenges are overcome and Bausch & Lomb continues its worldwide growth, it will be a very attractive asset to Valeant or others. A potential strategy for Valeant would be to spin-off a small percentage (20%-30%) of Bausch & Lomb via IPO and maintain control of the asset.

Disclosure: I am/we are long VRX.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

About this article:

Expand

Author payment: $35 + $0.01/page view. Authors of PRO articles receive a minimum guaranteed payment of $150-500. Become a contributor »

Tagged: Investing Ideas, Long Ideas, Healthcare, Drug Delivery & Accessories, Canada

Problem with this article? Please tell us. Disagree with this article? Submit your own.

T

guly

Forumer storico

Bonjour,

Comme prévue rien ne fait bouger le titre, je vous avez fait part de mon expérience et de mon analyse.

Depuis que les US via les privante equity sont entrés au capital de Nicox, il n'y aura aucune envolée du titre, même le jour de l'annonce FDA (positive je pense).

Pourquoi:

Le cahier des charges d'un private equity n'a absolument rien à voir avec une quelconque valorisation du cours de bourse.. ils s'en tamponne, leurs objectifs est la prise de participation et la main mise sur un pipeline.

Ils ont ensuite suffisamment de "connexion" avec Le Bras armé US (FDA) et tout est fait pour flinguer Nicox, il pourront aller jusqu'à un retrait pur et simple de la cote... étant au capital, il pourront quand Nicox sera quasi morte la revendre X 5 ou 20 et réaliser l'atteinte de l'objectif. IL FAUT INTERDIRE LES PRIVATES EQUITY;

Voilà pourquoi l'année dernière j'ai décidé de sortir de la valeur.

Bon courage

questo post mi sembra molto concreto e realistico,e' vero,quando entrano certi fondi il titolo non lo fanno alzare ma entrano per altri scopi.e di chi e' la colpa quando si fanno entrare certi fondi?il discorso vale anche per molmed anche se li SG piu' che un private equity sono strozzini di mercato.pero'nel 90 % dei casi e' cosi',ha perfettamente ragione questo tizio che scrive su boursorama.QUANDO CI SI METTE IN MANO A CERTA GENTE LO SI SA BENE COME VA A FINIRE.POI POSSONO FARE TUTTI I REPORT STRAPOSITIVI CHE VOGLIONO,MA SE C'E' QUALCUNO CHE DICE CHE NON DEVE SALIRE......NON SALE.

Comme prévue rien ne fait bouger le titre, je vous avez fait part de mon expérience et de mon analyse.

Depuis que les US via les privante equity sont entrés au capital de Nicox, il n'y aura aucune envolée du titre, même le jour de l'annonce FDA (positive je pense).

Pourquoi:

Le cahier des charges d'un private equity n'a absolument rien à voir avec une quelconque valorisation du cours de bourse.. ils s'en tamponne, leurs objectifs est la prise de participation et la main mise sur un pipeline.

Ils ont ensuite suffisamment de "connexion" avec Le Bras armé US (FDA) et tout est fait pour flinguer Nicox, il pourront aller jusqu'à un retrait pur et simple de la cote... étant au capital, il pourront quand Nicox sera quasi morte la revendre X 5 ou 20 et réaliser l'atteinte de l'objectif. IL FAUT INTERDIRE LES PRIVATES EQUITY;

Voilà pourquoi l'année dernière j'ai décidé de sortir de la valeur.

Bon courage

questo post mi sembra molto concreto e realistico,e' vero,quando entrano certi fondi il titolo non lo fanno alzare ma entrano per altri scopi.e di chi e' la colpa quando si fanno entrare certi fondi?il discorso vale anche per molmed anche se li SG piu' che un private equity sono strozzini di mercato.pero'nel 90 % dei casi e' cosi',ha perfettamente ragione questo tizio che scrive su boursorama.QUANDO CI SI METTE IN MANO A CERTA GENTE LO SI SA BENE COME VA A FINIRE.POI POSSONO FARE TUTTI I REPORT STRAPOSITIVI CHE VOGLIONO,MA SE C'E' QUALCUNO CHE DICE CHE NON DEVE SALIRE......NON SALE.

viralic

Forumer storico

Bonjour,

Comme prévue rien ne fait bouger le titre, je vous avez fait part de mon expérience et de mon analyse.

Depuis que les US via les privante equity sont entrés au capital de Nicox, il n'y aura aucune envolée du titre, même le jour de l'annonce FDA (positive je pense).

Pourquoi:

Le cahier des charges d'un private equity n'a absolument rien à voir avec une quelconque valorisation du cours de bourse.. ils s'en tamponne, leurs objectifs est la prise de participation et la main mise sur un pipeline.

Ils ont ensuite suffisamment de "connexion" avec Le Bras armé US (FDA) et tout est fait pour flinguer Nicox, il pourront aller jusqu'à un retrait pur et simple de la cote... étant au capital, il pourront quand Nicox sera quasi morte la revendre X 5 ou 20 et réaliser l'atteinte de l'objectif. IL FAUT INTERDIRE LES PRIVATES EQUITY;

Voilà pourquoi l'année dernière j'ai décidé de sortir de la valeur.

Bon courage

questo post mi sembra molto concreto e realistico,e' vero,quando entrano certi fondi il titolo non lo fanno alzare ma entrano per altri scopi.e di chi e' la colpa quando si fanno entrare certi fondi?il discorso vale anche per molmed anche se li SG piu' che un private equity sono strozzini di mercato.pero'nel 90 % dei casi e' cosi',ha perfettamente ragione questo tizio che scrive su boursorama.QUANDO CI SI METTE IN MANO A CERTA GENTE LO SI SA BENE COME VA A FINIRE.POI POSSONO FARE TUTTI I REPORT STRAPOSITIVI CHE VOGLIONO,MA SE C'E' QUALCUNO CHE DICE CHE NON DEVE SALIRE......NON SALE.

Mi pare che il titolo stia salendo..... ma forse a questo tipo che è uscito dal titolo gli brucia molto ...probabile che sia uscito a 8,40 a fine anno e ora dopo 2 mesi si trova con un euro in più...peggio per lui.....Guly, stai comodo e goditi la salita dei prossimi mesi.

p.s. Caro guly...faresti meglio anche a legger quando sono stati postati certi commenti.....ti saresti accorto che il post è del 9 marzo mattina......quando nicox quotava 8,70 euro........venerdi è arrivata ad 1 euro in più......ed il tipo penso sia molto incaxxato in quanto fuori dal titolo....o magari è rientrato a 9,50 !!!

Ultima modifica:

guly

Forumer storico

non lo so ma comunque l'ipotesi mi sembra realistica e lo sai bene anche tu,si vede chiaramente che non la fanno salire e vedremo in avanti.Mi pare che il titolo stia salendo..... ma forse a questo tipo che è uscito dal titolo gli brucia molto ...probabile che sia uscito a 8,40 a fine anno e ora dopo 2 mesi si trova con un euro in più...peggio per lui.....Guly, stai comodo e goditi la salita dei prossimi mesi.

p.s. Caro guly...faresti meglio anche a legger quando sono stati postati certi commenti.....ti saresti accorto che il post è del 9 marzo mattina......quando nicox quotava 8,70 euro........venerdi è arrivata ad 1 euro in più......ed il tipo penso sia molto incaxxato in quanto fuori dal titolo....o magari è rientrato a 9,50 !!!

Gia' lunedi' si vedra',se continua a salire senza ritracciamenti (come ha fatto sempre ultimamente) avrai ragione altrimenti e' giusta l'ipotesi postata dal forumista di boursorama.Ormai avrai ben capito che in borsa regali non se ne fanno piu' come una volta,rialzi come quelli che portarono nicox da 7 euro a 23 penso siano ormai non piu' realistici di questi tempi.

viralic

Forumer storico

non lo so ma comunque l'ipotesi mi sembra realistica e lo sai bene anche tu,si vede chiaramente che non la fanno salire e vedremo in avanti.

Gia' lunedi' si vedra',se continua a salire senza ritracciamenti (come ha fatto sempre ultimamente) avrai ragione altrimenti e' giusta l'ipotesi postata dal forumista di boursorama.Ormai avrai ben capito che in borsa regali non se ne fanno piu' come una volta,rialzi come quelli che portarono nicox da 7 euro a 23 penso siano ormai non piu' realistici di questi tempi.

vedremo....

guly

Forumer storico

vedremo....

comunque spero che sbaglio io e non sia cosi' visto che ho qualche nicox e vorrei uscire almeno a 13 euro.li sinceramente mi contento e chiudo il discorso con la cloaca chiamata eufemisticamente borsa valori.mi viene da ridere a leggere questa dicitura,specialmente se la raffornto con quella di milano che piu' che una borsa valori mi sembra una discarica di immondizia.

Similar threads

Pharma e Biotech - Europa

NicOx..aspettando non si sa cosa..senza il NET-ZOHAR!!

- Risposte

- 35

- Visite

- 6.020

Users who are viewing this thread

Total: 1 (members: 0, guests: 1)