Stai usando un browser molto obsoleto. Puoi incorrere in problemi di visualizzazione di questo e altri siti oltre che in problemi di sicurezza. .

Dovresti aggiornarlo oppure usarne uno alternativo, moderno e sicuro.

Dovresti aggiornarlo oppure usarne uno alternativo, moderno e sicuro.

Analisi Intermarket ....quelli che.... Investire&tradare - Cap. 2

- Creatore Discussione Dogtown

- Data di Inizio

:sorpresa:

:sorpresa: :yeah:

:yeah:

kuelo

C'e' grosssa crise...

certo che interessa kuelo...quindi ci sfasciamo per chiudere il tutto con un ritorno verso il minimo precedente, i tempi dell'attuazione?

Grazie per le tue analisi")

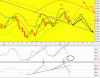

...forse avevi letto solo il primo post...in quello dopo c'era il previsionale ...che piu' o meno e' quello che avevo messo dopo la prima settimana di marzo...non cambia niente...il percorso e' quello nero....ripeto....e' un previsonale...non e' che andra' cosi' esattamente ehhh

...il terzo apice potra' essere un po' piu' alto della quota indicata o un po' piu' basso , lo controlleremo passo - passo ...l'unica condizione e' che quel minimo del 5 aprile non venga rotto al riba entro 8 gg di borsa circa...allora dovro' rimodellarlo

...il terzo apice potra' essere un po' piu' alto della quota indicata o un po' piu' basso , lo controlleremo passo - passo ...l'unica condizione e' che quel minimo del 5 aprile non venga rotto al riba entro 8 gg di borsa circa...allora dovro' rimodellarlo..e' tutto uguale..e lo sviluppo di quello in allegato qui...l'oscillatore sotto ha infrociato al rialzo ( seppur un po' in anticipo

coi prezzi )ma come dico da un po' "siamo nel tempo del rialzo" di medio-breve...che pero' ad ora ha dimostrato una certa debolezza ...quindi il target del rimbalzo...massimo...che dovremmo fare tra maggio e giugno ( ma forse piu' maggio ) .ad ora retsa in area 16400 ( max 16600)...ma anche questo vedro' di affinarlo con il passare del tempo

coi prezzi )ma come dico da un po' "siamo nel tempo del rialzo" di medio-breve...che pero' ad ora ha dimostrato una certa debolezza ...quindi il target del rimbalzo...massimo...che dovremmo fare tra maggio e giugno ( ma forse piu' maggio ) .ad ora retsa in area 16400 ( max 16600)...ma anche questo vedro' di affinarlo con il passare del tempoinsomma sono contrario di fondo a chi ci vede a 20000 o giu' di li a fine anno...non solo per il nostro...ma anche guardando sp e dax

di sp gia' detto 1000 volte ..( ma non e' ancora "maturo" per cadere dall'albero.for me )...il dax effettivamente lo "conosco" meno...e' nel suo secondo intermedio( sono entrambi indietro come tempo rispetto a noi ..loro chiuderanno l'annuale st'inverno...noi a cavallod ell'estate)...ha un vincolo al ribasso...e forse ancora un po' di strada da fare in giu'....ma sia li che su sp mi aspetto poi un mini pulbekko...inferiore al max degli 8000 e spicci ..magari sui 7800...

...ma il dax ha gia' 4/5 di figura ribassisita di lungo completati...( je manca l'ultima botta ..il su e giu' finale )...sp e' solo a meta'........ripeto...questo e' solo il mio pensiero..se altri la vedono in altro modo e voglion mettere due scarabocchi....ma vedo che a parte qualcuno...( LUPONE; GIPONE, 99; ) non si palesa mai nessuno

Allegati

kuelo

C'e' grosssa crise...

infine per l'ultima volta ( dalla prossima sarete autorizzati a prendermi a selciate  erichiamarmi all'ordini...anzi ..vi prego di farlo )

erichiamarmi all'ordini...anzi ..vi prego di farlo )

vorrei dire due cose politiche

evviva' le NOVITA'

GIORGIO NAPOLITANO...e' il nuovo che avanza

avevan chiesto anche a Matusalemme...ma ha detto che effettivamente era un po' vecchio e non se la sentiva

e forse AMATO PRESIDENTE

complimenti ...a TUTTI GLI ELETTORI DI PD E PDL

IL PD...una manica di incapaci col paraocchi candidati al suicido

IL PDL...quanto son lontani quei gg in cui Il nano malefico usciva nascosto nell'auto blu dal palazzo deriso , sbeffeggiatto da mezza italia / e da tutto il mondo)..tra le scene dementi di euforia di piazza e io a dirvi....

" attenti che quello torna"...

e infatti......eccolo li il pappone..che se la ride alle cene...gia sta pregustando , da grandissimo sta...tista di MINKIA ..le prossime mosse per tornare a farci fare le solite ( o forse ancora meglio ) figure da deficenti in tutta europa e oltre

saran di nuovo le corna nelle foto? urlare come una gallina per richiamare OBAMA, telefonare in questura per salvare la zia di Hollande?

urlare come una gallina per richiamare OBAMA, telefonare in questura per salvare la zia di Hollande?

etc etc....nessuno puo' saperlo

ma va bene cosi'..e ' quello che ci meritiamo

solo un mesetto fa il 60% del paese havotato per questa bella gente...

e non sono d'accordo con chi dice che se ne va dall'ITALIA perche' e' un paese di mierda( ma non era un'altra delle perle del ns premierissimo incatramatoputtanierediminorenni?....:Y:Y:Y)

il paese ITALIA e' bellissimo..forse c'e solo troppa gente di mierda...

e l'ignoranza non e' una scusa....

vorrei dire due cose politiche

evviva' le NOVITA'

GIORGIO NAPOLITANO...e' il nuovo che avanza

avevan chiesto anche a Matusalemme...ma ha detto che effettivamente era un po' vecchio e non se la sentiva

e forse AMATO PRESIDENTE

complimenti ...a TUTTI GLI ELETTORI DI PD E PDL

IL PD...una manica di incapaci col paraocchi candidati al suicido

IL PDL...quanto son lontani quei gg in cui Il nano malefico usciva nascosto nell'auto blu dal palazzo deriso , sbeffeggiatto da mezza italia / e da tutto il mondo

)..tra le scene dementi di euforia di piazza e io a dirvi...." attenti che quello torna"...

e infatti....

..eccolo li il pappone..che se la ride alle cene...gia sta pregustando , da grandissimo sta...tista di MINKIA ..le prossime mosse per tornare a farci fare le solite ( o forse ancora meglio ) figure da deficenti in tutta europa e oltresaran di nuovo le corna nelle foto?

urlare come una gallina per richiamare OBAMA, telefonare in questura per salvare la zia di Hollande?etc etc....nessuno puo' saperlo

ma va bene cosi'..e ' quello che ci meritiamo

solo un mesetto fa il 60% del paese havotato per questa bella gente...

e non sono d'accordo con chi dice che se ne va dall'ITALIA perche' e' un paese di mierda

....:Y:Y:Y)il paese ITALIA e' bellissimo

..forse c'e solo troppa gente di mierda...e l'ignoranza non e' una scusa....

Ultima modifica:

DDUKE

Viva i popoli, Viva le Nazioni europee, fanculo U€

La guerra è ancora lunga, come tutte, o quasi, le guerre.

Certo è che finalmente hanno gettato tutti la maschera, sopratutto i dirigenti del'ex PC.

Va detto che, secondo me, c'è un altro problema che va oltre la complicità tra PD e PDL è che lo si può intuire sulla mancanza di pressione fatta dal PDL sul PD per il caso MPS. Nessuno si è chiesto come mai il nano non ha infierito sul caso MPS ? non vi è apparso strano ???

Evidentemente il nano tiene per le palle la vecchia classe di dirigenti del PD, ha la chiave dell'armadio degli orrori, quindi non è solo complicità perchè altrimenti non ci sarebbe stata nessuna spaccatura nel loro partito.

Credo che il buon Craxi abbia lasciato un bel pò di roba al nano per difendersi. Quindi prima si spazza via il PD e prima il nano finirà di esistere visto che non potrà ricattare nessuno.

La successiva domanda è :

può il nano fare l'errore assoluto ? nominare il topo Presidente del Consiglio o dell'Economia ???

Se ciò avvenisse l'unica spiegazione sarà il delirio di onnipotenza del nano che , dopo il PdR, a vederlo sugli spalti, è sembrato al settimo cielo, tra risate e barzellette.

La domanda, l'unica domanda in essere pèrò rimane PERCHE' NON RODOTA'. Quanta paura aveva il PD di Rodotà, perchè ? cosa c'è di così tanto SPAVENTEVOLE negli armadi dell'ex PC ?

Lo sappiamo tutti cosa c'è, lo vedono tutti i cittadini che vivono in Regioni e Province dove da sempre esiste un solo partito dal 45 in su.

La guerra è ancora lunga.

Certo è che finalmente hanno gettato tutti la maschera, sopratutto i dirigenti del'ex PC.

Va detto che, secondo me, c'è un altro problema che va oltre la complicità tra PD e PDL è che lo si può intuire sulla mancanza di pressione fatta dal PDL sul PD per il caso MPS. Nessuno si è chiesto come mai il nano non ha infierito sul caso MPS ? non vi è apparso strano ???

Evidentemente il nano tiene per le palle la vecchia classe di dirigenti del PD, ha la chiave dell'armadio degli orrori, quindi non è solo complicità perchè altrimenti non ci sarebbe stata nessuna spaccatura nel loro partito.

Credo che il buon Craxi abbia lasciato un bel pò di roba al nano per difendersi. Quindi prima si spazza via il PD e prima il nano finirà di esistere visto che non potrà ricattare nessuno.

La successiva domanda è :

può il nano fare l'errore assoluto ? nominare il topo Presidente del Consiglio o dell'Economia ???

Se ciò avvenisse l'unica spiegazione sarà il delirio di onnipotenza del nano che , dopo il PdR, a vederlo sugli spalti, è sembrato al settimo cielo, tra risate e barzellette.

La domanda, l'unica domanda in essere pèrò rimane PERCHE' NON RODOTA'. Quanta paura aveva il PD di Rodotà, perchè ? cosa c'è di così tanto SPAVENTEVOLE negli armadi dell'ex PC ?

Lo sappiamo tutti cosa c'è, lo vedono tutti i cittadini che vivono in Regioni e Province dove da sempre esiste un solo partito dal 45 in su.

La guerra è ancora lunga.

Dogtown

Forever Ultras Ghetto

La guerra è ancora lunga, come tutte, o quasi, le guerre.

Certo è che finalmente hanno gettato tutti la maschera, sopratutto i dirigenti del'ex PC.

Va detto che, secondo me, c'è un altro problema che va oltre la complicità tra PD e PDL è che lo si può intuire sulla mancanza di pressione fatta dal PDL sul PD per il caso MPS. Nessuno si è chiesto come mai il nano non ha infierito sul caso MPS ? non vi è apparso strano ???

Evidentemente il nano tiene per le palle la vecchia classe di dirigenti del PD, ha la chiave dell'armadio degli orrori, quindi non è solo complicità perchè altrimenti non ci sarebbe stata nessuna spaccatura nel loro partito.

Credo che il buon Craxi abbia lasciato un bel pò di roba al nano per difendersi. Quindi prima si spazza via il PD e prima il nano finirà di esistere visto che non potrà ricattare nessuno.

La successiva domanda è :

può il nano fare l'errore assoluto ? nominare il topo Presidente del Consiglio o dell'Economia ???

Se ciò avvenisse l'unica spiegazione sarà il delirio di onnipotenza del nano che , dopo il PdR, a vederlo sugli spalti, è sembrato al settimo cielo, tra risate e barzellette.

La domanda, l'unica domanda in essere pèrò rimane PERCHE' NON RODOTA'. Quanta paura aveva il PD di Rodotà, perchè ? cosa c'è di così tanto SPAVENTEVOLE negli armadi dell'ex PC ?

Lo sappiamo tutti cosa c'è, lo vedono tutti i cittadini che vivono in Regioni e Province dove da sempre esiste un solo partito dal 45 in su.

La guerra è ancora lunga.

Novenove

Moderator

Tanto va la gatta al lardo....

Bell articolo:

Per far riprendere il mercato immobiliare le banche devono ricominciare a concedere mutui a porci e cani. Ma con una sostanziale differenza...

Pensavate che fosse possibile, per i governi occidentali, imparare una lezione dopo una batosta storica che ha quasi messo in ginocchio interi continenti? Ebbene: sbagliato. Non si impara mai nulla.

D'altronde quando si aderisce ciecamente ad una dottrina che non richiede neppure di essere capita, questi sono rischi che si corrono. Ricordate ad esempio il disastro dei mutui facili? Se a un qualsiasi cittadino in strada menzionate le parole "mutui subprime", inorridisce, si segna e invoca i santi: anche i bambini sanno infatti che all'origine della crisi mondiale, specialmente dal lato americano dell'Atlantico, c'è lo scandalo dei subprime elargiti a piene mani e che alla fine hanno causato crash di banche e conseguenti pesantissimi bailout. Se ne è parlato a iosa.

E' passato appena qualche anno, siamo ancora in mezzo al guado (senza sapere neppure se ne usciremo) e Obama cosa fa? Per stimolare l'economia... invita le banche ad elargire mutui anche a chi non può pagare.

Per i numerosi increduli, ecco la fedele traduzione e il link al Washington Post:

L'amministrazione Obama spinge le banche a concedere mutui anche alle persone con poca affidabilità creditizia.

E' uno sforzo che gli esperti credono aiuterà la ripresa dell'economia, ma che gli scettici sostengono aprirà le porte ai prestiti rischiosi che hanno già causato il crash immobiliare. Gli addetti dell'amministrazione garantiscono di stare lavorando affinché le banche prestino a un più vasto numero di persone avvantaggiandosi dei programmi pubblici che assicurano i mutui contro il default.

Si sta anche pressando il Dipartimento della Giustizia perché fornisca assicurazioni alle banche, diventate molto caute, che non dovranno affrontare problemi legali o finanziari se concederanno mutui ai clienti a rischio che oggi corrispondono agli standard ma che un domani andranno in bancarotta.

Insomma, se si è capito l'oscuro linguaggio politico-legale: per far riprendere il mercato immobiliare le banche devono ricominciare a concedere mutui a porci e cani. Con la differenza che, se stavolta va di nuovo tutto a gambe all'aria, lo Stato tampona coi soldi pubblici e le banche la passano liscia.

E noi che credevamo che non avessero imparato la lezione: l'hanno imparata eccome.

Bell articolo:

Per far riprendere il mercato immobiliare le banche devono ricominciare a concedere mutui a porci e cani. Ma con una sostanziale differenza...

Pensavate che fosse possibile, per i governi occidentali, imparare una lezione dopo una batosta storica che ha quasi messo in ginocchio interi continenti? Ebbene: sbagliato. Non si impara mai nulla.

D'altronde quando si aderisce ciecamente ad una dottrina che non richiede neppure di essere capita, questi sono rischi che si corrono. Ricordate ad esempio il disastro dei mutui facili? Se a un qualsiasi cittadino in strada menzionate le parole "mutui subprime", inorridisce, si segna e invoca i santi: anche i bambini sanno infatti che all'origine della crisi mondiale, specialmente dal lato americano dell'Atlantico, c'è lo scandalo dei subprime elargiti a piene mani e che alla fine hanno causato crash di banche e conseguenti pesantissimi bailout. Se ne è parlato a iosa.

E' passato appena qualche anno, siamo ancora in mezzo al guado (senza sapere neppure se ne usciremo) e Obama cosa fa? Per stimolare l'economia... invita le banche ad elargire mutui anche a chi non può pagare.

Per i numerosi increduli, ecco la fedele traduzione e il link al Washington Post:

L'amministrazione Obama spinge le banche a concedere mutui anche alle persone con poca affidabilità creditizia.

E' uno sforzo che gli esperti credono aiuterà la ripresa dell'economia, ma che gli scettici sostengono aprirà le porte ai prestiti rischiosi che hanno già causato il crash immobiliare. Gli addetti dell'amministrazione garantiscono di stare lavorando affinché le banche prestino a un più vasto numero di persone avvantaggiandosi dei programmi pubblici che assicurano i mutui contro il default.

Si sta anche pressando il Dipartimento della Giustizia perché fornisca assicurazioni alle banche, diventate molto caute, che non dovranno affrontare problemi legali o finanziari se concederanno mutui ai clienti a rischio che oggi corrispondono agli standard ma che un domani andranno in bancarotta.

Insomma, se si è capito l'oscuro linguaggio politico-legale: per far riprendere il mercato immobiliare le banche devono ricominciare a concedere mutui a porci e cani. Con la differenza che, se stavolta va di nuovo tutto a gambe all'aria, lo Stato tampona coi soldi pubblici e le banche la passano liscia.

E noi che credevamo che non avessero imparato la lezione: l'hanno imparata eccome.

f4f

翠鸟科

Bell articolo:

Per far riprendere il mercato immobiliare le banche devono ricominciare a concedere mutui a porci e cani. Ma con una sostanziale differenza...

Pensavate che fosse possibile, per i governi occidentali, imparare una lezione dopo una batosta storica che ha quasi messo in ginocchio interi continenti? Ebbene: sbagliato. Non si impara mai nulla.

D'altronde quando si aderisce ciecamente ad una dottrina che non richiede neppure di essere capita, questi sono rischi che si corrono. Ricordate ad esempio il disastro dei mutui facili? Se a un qualsiasi cittadino in strada menzionate le parole "mutui subprime", inorridisce, si segna e invoca i santi: anche i bambini sanno infatti che all'origine della crisi mondiale, specialmente dal lato americano dell'Atlantico, c'è lo scandalo dei subprime elargiti a piene mani e che alla fine hanno causato crash di banche e conseguenti pesantissimi bailout. Se ne è parlato a iosa.

E' passato appena qualche anno, siamo ancora in mezzo al guado (senza sapere neppure se ne usciremo) e Obama cosa fa? Per stimolare l'economia... invita le banche ad elargire mutui anche a chi non può pagare.

Per i numerosi increduli, ecco la fedele traduzione e il link al Washington Post:

L'amministrazione Obama spinge le banche a concedere mutui anche alle persone con poca affidabilità creditizia.

E' uno sforzo che gli esperti credono aiuterà la ripresa dell'economia, ma che gli scettici sostengono aprirà le porte ai prestiti rischiosi che hanno già causato il crash immobiliare. Gli addetti dell'amministrazione garantiscono di stare lavorando affinché le banche prestino a un più vasto numero di persone avvantaggiandosi dei programmi pubblici che assicurano i mutui contro il default.

Si sta anche pressando il Dipartimento della Giustizia perché fornisca assicurazioni alle banche, diventate molto caute, che non dovranno affrontare problemi legali o finanziari se concederanno mutui ai clienti a rischio che oggi corrispondono agli standard ma che un domani andranno in bancarotta.

Insomma, se si è capito l'oscuro linguaggio politico-legale: per far riprendere il mercato immobiliare le banche devono ricominciare a concedere mutui a porci e cani. Con la differenza che, se stavolta va di nuovo tutto a gambe all'aria, lo Stato tampona coi soldi pubblici e le banche la passano liscia.

E noi che credevamo che non avessero imparato la lezione: l'hanno imparata eccome.

opoVca miseVia ... propriuo adesso che mi ero convinto che peggio dei nostri politici fosse del tutto impossibbile

Novenove

Moderator

Bell articolo:

Per far riprendere il mercato immobiliare le banche devono ricominciare a concedere mutui a porci e cani. Ma con una sostanziale differenza...

Pensavate che fosse possibile, per i governi occidentali, imparare una lezione dopo una batosta storica che ha quasi messo in ginocchio interi continenti? Ebbene: sbagliato. Non si impara mai nulla.

D'altronde quando si aderisce ciecamente ad una dottrina che non richiede neppure di essere capita, questi sono rischi che si corrono. Ricordate ad esempio il disastro dei mutui facili? Se a un qualsiasi cittadino in strada menzionate le parole "mutui subprime", inorridisce, si segna e invoca i santi: anche i bambini sanno infatti che all'origine della crisi mondiale, specialmente dal lato americano dell'Atlantico, c'è lo scandalo dei subprime elargiti a piene mani e che alla fine hanno causato crash di banche e conseguenti pesantissimi bailout. Se ne è parlato a iosa.

E' passato appena qualche anno, siamo ancora in mezzo al guado (senza sapere neppure se ne usciremo) e Obama cosa fa? Per stimolare l'economia... invita le banche ad elargire mutui anche a chi non può pagare.

Per i numerosi increduli, ecco la fedele traduzione e il link al Washington Post:

L'amministrazione Obama spinge le banche a concedere mutui anche alle persone con poca affidabilità creditizia.

E' uno sforzo che gli esperti credono aiuterà la ripresa dell'economia, ma che gli scettici sostengono aprirà le porte ai prestiti rischiosi che hanno già causato il crash immobiliare. Gli addetti dell'amministrazione garantiscono di stare lavorando affinché le banche prestino a un più vasto numero di persone avvantaggiandosi dei programmi pubblici che assicurano i mutui contro il default.

Si sta anche pressando il Dipartimento della Giustizia perché fornisca assicurazioni alle banche, diventate molto caute, che non dovranno affrontare problemi legali o finanziari se concederanno mutui ai clienti a rischio che oggi corrispondono agli standard ma che un domani andranno in bancarotta.

Insomma, se si è capito l'oscuro linguaggio politico-legale: per far riprendere il mercato immobiliare le banche devono ricominciare a concedere mutui a porci e cani. Con la differenza che, se stavolta va di nuovo tutto a gambe all'aria, lo Stato tampona coi soldi pubblici e le banche la passano liscia.

E noi che credevamo che non avessero imparato la lezione: l'hanno imparata eccome.

Inside the Boston Marathon probe

After capture, a search for motives

PHOTOS | Boston’s harrowing week

Boston suspect's YouTube playlist evolved...

Obama administration pushes banks to make home loans to people with weaker credit

View Photo Gallery — Obama administration struggles to help homeowners: A look at the Obama administration’s efforts in trying to help homeowners and bring the nation out of its housing slump.

By Zachary A. Goldfarb, Published: April 3

The Obama administration is engaged in a broad push to make more home loans available to people with weaker credit, an effort that officials say will help power the economic recovery but that skeptics say could open the door to the risky lending that caused the housing crash in the first place.

President Obama’s economic advisers and outside experts say the nation’s much-celebrated housing rebound is leaving too many people behind, including young people looking to buy their first homes and individuals with credit records weakened by the recession.

More business news

Fannie Mae reports $7.6 billion profit in fourth quarter

Zachary A. Goldfarb APR 3

Fannie and Freddie Mac have enjoyed an unexpected resurgence as the housing market recovers.

GAO: Money management firms offer workers misleading 401(k) advice

Michael A. Fletcher APR 3

Report to be released today says workers are encouraged to invest in accounts with higher fees.

The case for expanding Social Security

Brad Plumer APR 3

The New America Foundation is proposing a big new expansion of Social Security, instead of the usual ideas for cuts. The reason? Our existing retirement system is broken.

Time to improve your financial knowledge

Michelle Singletary APR 3

It’s time to stop worrying about a lack of savings and do something about it.

In response, administration officials say they are working to get banks to lend to a wider range of borrowers by taking advantage of taxpayer-backed programs — including those offered by the Federal Housing Administration — that insure home loans against default.

Housing officials are urging the Justice Department to provide assurances to banks, which have become increasingly cautious, that they will not face legal or financial recriminations if they make loans to riskier borrowers who meet government standards but later default.

Officials are also encouraging lenders to use more subjective judgment in determining whether to offer a loan and are seeking to make it easier for people who owe more than their properties are worth to refinance at today’s low interest rates, among other steps.

Obama pledged in his State of the Union address to do more to make sure more Americans can enjoy the benefits of the housing recovery, but critics say encouraging banks to lend as broadly as the administration hopes will sow the seeds of another housing disaster and endanger taxpayer dollars.

“If that were to come to pass, that would open the floodgates to highly excessive risk and would send us right back on the same path we were just trying to recover from,” said Ed Pinto, a resident fellow at the American Enterprise Institute and former top executive at mortgage giant Fannie Mae.

Administration officials say they are looking only to allay unnecessary hesitation among banks and encourage safe lending to borrowers who have the financial wherewithal to pay.

“There’s always a tension that you have to take seriously between providing clarity and rules of the road and not giving any opportunity to restart the kind of irresponsible lending that we saw in the mid-2000s,” said a senior administration official who was not authorized to speak on the record.

The administration’s efforts come in the midst of a housing market that has been surging for the past year but that has been delivering most of the benefits to established homeowners with high credit scores or to investors who have been behind a significant number of new purchases.

“If you were going to tell people in low-income and moderate-income communities and communities of color there was a housing recovery, they would look at you as if you had two heads,” said John Taylor, president of the National Community Reinvestment Coalition, a nonprofit housing organization. “It is very difficult for people of low and moderate incomes to refinance or buy homes.”

Novenove

Moderator

opoVca miseVia ... propriuo adesso che mi ero convinto che peggio dei nostri politici fosse del tutto impossibbile

Ciao caro, esco a bere un aperitivo va

f4f

翠鸟科

Ciao caro, esco a bere un aperitivo va

beatto te ... io devo sbrigare una cosa per domani

bevi anche per me

")

Similar threads

Users who are viewing this thread

Total: 1 (members: 0, guests: 1)