solointraday

Forumer storico

Tanto gentile e tanto onesta pareIs the bullish market creating a volatility anomaly? - New paradigm or short

term anomaly?

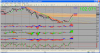

In these last few days we are seeing an “inverse” relationship between spot and

implied volatility. In normal market conditions as market moves up the

volatility tends to decrease inversely. In the last 3 days, though, both the

spot and volatility on the S&P500 have been moving up. Some are talking about a

new paradigm, but actually the only paradigm is a current low volatility

environment combined with a flow of investors buying upside calls provided by a

bullish market sentiment.

Some of the explanations lead to investor concerns for potential downside

corrections. Upside calls provide upside exposure while limiting a potential

correction. A second reason may also be a simple technical effect: with

volatility so low, even if spot keeps increasing, the implied volatility does

not move down further.

la donna mia quand’ella altrui saluta,

ch’ogne lingua deven tremando muta,

e li occhi no l’ardiscon di guardare.

ci sarò

ci sarò

")

a contatto con la shiff

a contatto con la shiff