http://seekingalpha.com/article/3978755-banco-populars-capital-raising-wake-call-european-banks

Banco Popular's Capital Raising: A Wake-Up Call For European Banks

May 31, 2016 9:47 AM ET

|

About:

Banco Popular (BPESF),

BPESY, Includes:

BBVA,

DB,

SAN,

UNCFF

Renaissance Research

⊕Follow(75 followers)

Long/short equity, banks

Send Message

Summary

Banco Popular surprised the market with a EUR2.5bn rights issue.

The stock declined by 27% after the announcement.

This is a brutal lesson for those, who go bottom-fishing in European banks.

On May 26, Banco Popular (

OTCPK PESY

PESY) (

OTCPKPESF), the fourth largest banking group in Spain, surprised the market with a EUR2.5bn rights issue and a fresh round of provisions for its troubled property portfolio.

To recap, last month, the group's CEO

Francisco Gomez said the bank had a very comfortable capital position.

Here is a quote from the 1Q16 conference call

To finish off talking to our about the highlights of this quarter, let me underscore the good position of Banco both as regards liquidity and capital compared to the same period of the last financial year 2015. Popular has brought its loan to deposit ratio down by 531 basis point, is now 107%.

Common Equity Tier 1 phased-in capital ratio is stand now at 12.81% and the fully loaded capital ratio 11.10% that's 56 basis points more than in the first quarter 2015.

The announcement really came as a surprise. The stock declined by 27%

Source: Bloomberg

Source: Bloomberg

Here is the transaction terms from Blooomberg:

- Capital increase to be carried out via issuing ~2b new ordinary shares at a subscription price of EUR1.25 for each new share;

- Discount is ~47% to yesterday's closing price of EUR2.36;

- Transaction size of ~EUR2.5bn compares to ~EUR5.2bn market cap as of yesterday's close;

- Issue ratio: 13 new shares for 14 existing shares according to terms

According the

bank's presentation, "some uncertainties could give rise to up to €4.7bn of additional provisions during 2016, mainly relating to credit and foreclosed assets, which could lead to accounting losses (covered, in terms of solvency, by the rights issue ) and the temporary suspension of dividend payments".

One important thing to note is that Banco Popular has successfully passed

the ECB's 2014 stress test.

What does this mean for the European banking sector?

Given the Banco Popular's CET1 ratio was well above its regulatory minimum requirement and the bank has successfully passed the ECB's 2014 stress test, we think the market will now focus on European banks with weak capital adequacy ratios. Moreover, we would not rule out that the ongoing capital debates could reach the point, where the market starts pricing in a capital call at some banks.

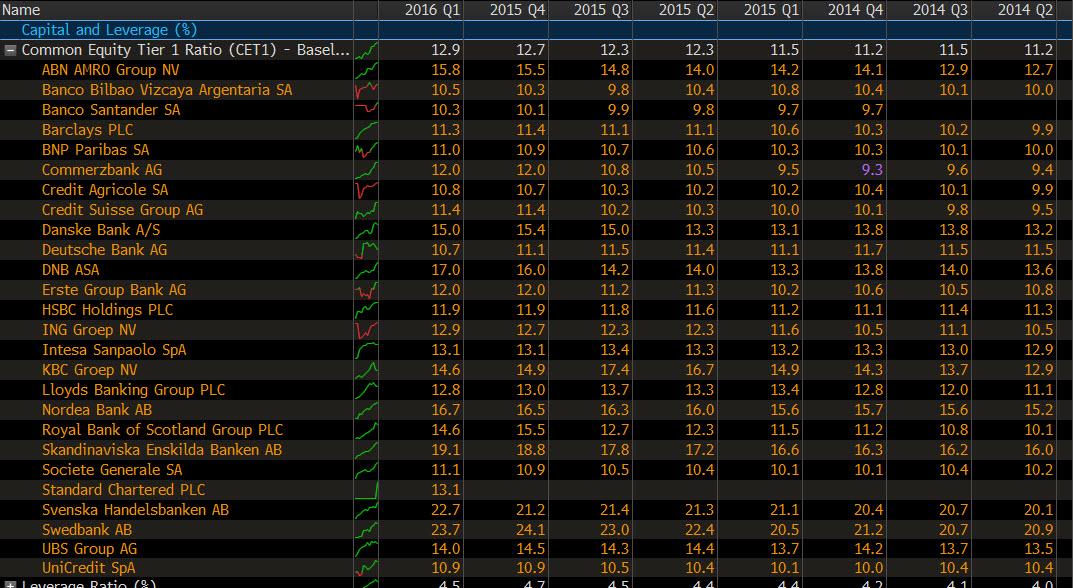

The table below shows that Banco Santander (NYSE:

SAN), BBVA (NYSE:

BBVA), Deutsche Bank (NYSE:

DB) and UniCredit (

OTCPK:UNCFF) have weak capital positions and we believe the market will definitely increase scrutiny on those names after Banco Popular's rights issue.

Source: Bloomberg

Source: Bloomberg

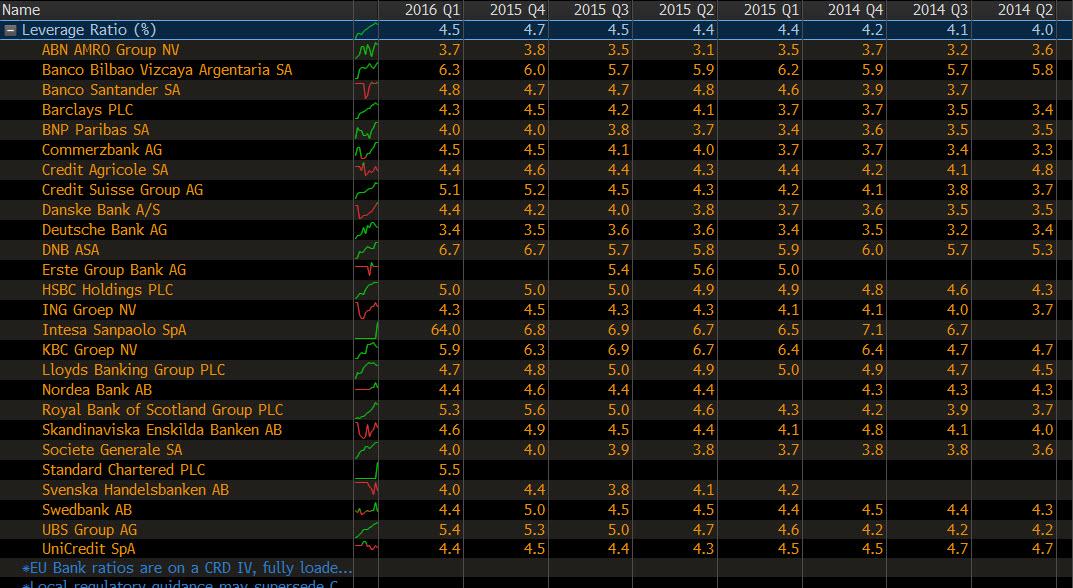

The leverage ratio is also an important indicator worth keeping eye on:

Source: Bloomberg

Bottom line

Source: Bloomberg

Bottom line

Banco Popular's rights issue has confirmed our view. Hence, we are reiterating our recommendation: Despite eye-popping low multiples, investors should avoid European banks with weak capital adequacy ratios, as organic capital generation will remain subdued and insufficient due to the low/negative interest environment. As a reminder, should a dirt cheap bank do a capital raising, an EPS dilution

would be devastating.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.